Many suspected the U.S. hard red winter wheat crop was in bad shape following months of drought across the Southern Plains. Few foresaw it getting this bad.

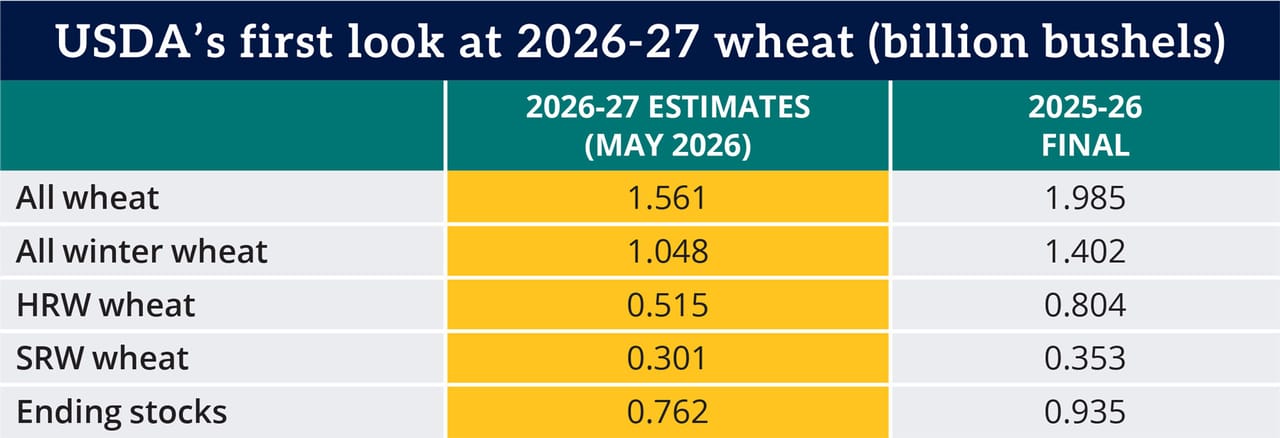

USDA shocked the grain trade in early May when it forecast the 2026-27 overall winter wheat harvest at 1.048 billion bushels, down 25% from the 2025-26 crop and the smallest since 1965. USDA’s initial estimate came in about 160 million bushels below the average analyst forecast.

Hard red winter wheat — the crop hardest hit by drought in the prime growing areas of western Kansas, eastern Colorado and the Panhandle region — was pegged at 514.8 million bushels, down 36% from last year.

Wheat futures started rallying early this year, and USDA’s May Crop Production report sent prices further skyward. On May 13, July HRW futures reached $7.50 per bushel, the highest intraday price for the most-active HRW contract since September 2023.

The World Agricultural Supply and Demand Estimates, released the same day, was a first peek into the agency’s expectations for the 2026-27 crop year. While the numbers are preliminary and likely to be revised throughout the coming year, wheat farmers could still glean at least four takeaways:

1. No rain, no grain. Over the winter and early spring, weather forecasts frequently teased rain relief for the Plains. More often than not, it never showed up. Most of the Panhandle region remained in extreme drought through mid-May, based on the U.S. Drought Monitor. Western Kansas was in moderate to severe drought. Yield prospects suffered accordingly, with USDA projecting Kansas to harvest an average of just 37 bushels per acre, down from 51 bpa in 2025.

2. Stocks poised to tighten. Smaller crops expected in the U.S. as well as other top producers including Argentina, Australia and Canada should shrink the global balance sheet, offering some hope for higher prices for farmers with wheat to sell. U.S. stocks at the end of 2026-27 are seen falling 17% to 775 million bushels, a three-year low. Global stocks are expected to drop 1.5%.

3. Exports fall. It’s a familiar bugaboo for U.S. wheat growers: Market rallies are nice, but they also make U.S. grain less competitive on a global market with many suppliers and no shortages — yet. That’s what happened this spring, as U.S. winter wheat values vaulted well above those of Russia. USDA forecasts 2026-27 U.S. wheat exports will drop 15% from a five-year high in 2025-26, to 762 million bushels.

4. Catch a good price. The drought-driven rally surely presented some enticing pricing opportunities for U.S. wheat farmers. USDA sees the average U.S. farm price for wheat surging to $6.50 in 2026-27, up $1.50 from 2025-26.

Some analysts see potential for further upside if the crop continues to shrink. But trying to pick tops is always risky in a market where speculative funds move in and out with lightning speed. Proceed with caution.

“When markets get ‘parabolic’ and funds are caught short, it’s impossible to outguess how high a market needs to go. Wheat can move ‘dollars’ in a hurry,” said Brady Huck, a principal and adviser at Empower Ag Trading. He cautioned that wheat rallies “tend to fade fast. It seems to me that funds don’t like holding on to long wheat positions and would rather be short.”