It may have gotten lost in the daily barrage of Iran war and $100 crude oil headlines, but the corn market once again has been quietly building a wider and wider carry structure while showing longer-term signs that the $5 mark could be settled in for a long visit.

For much of the spring, carry — the premium deferred futures contracts hold over nearer-term counterparts — expanded, reaching multiple-month or multiple-year highs.

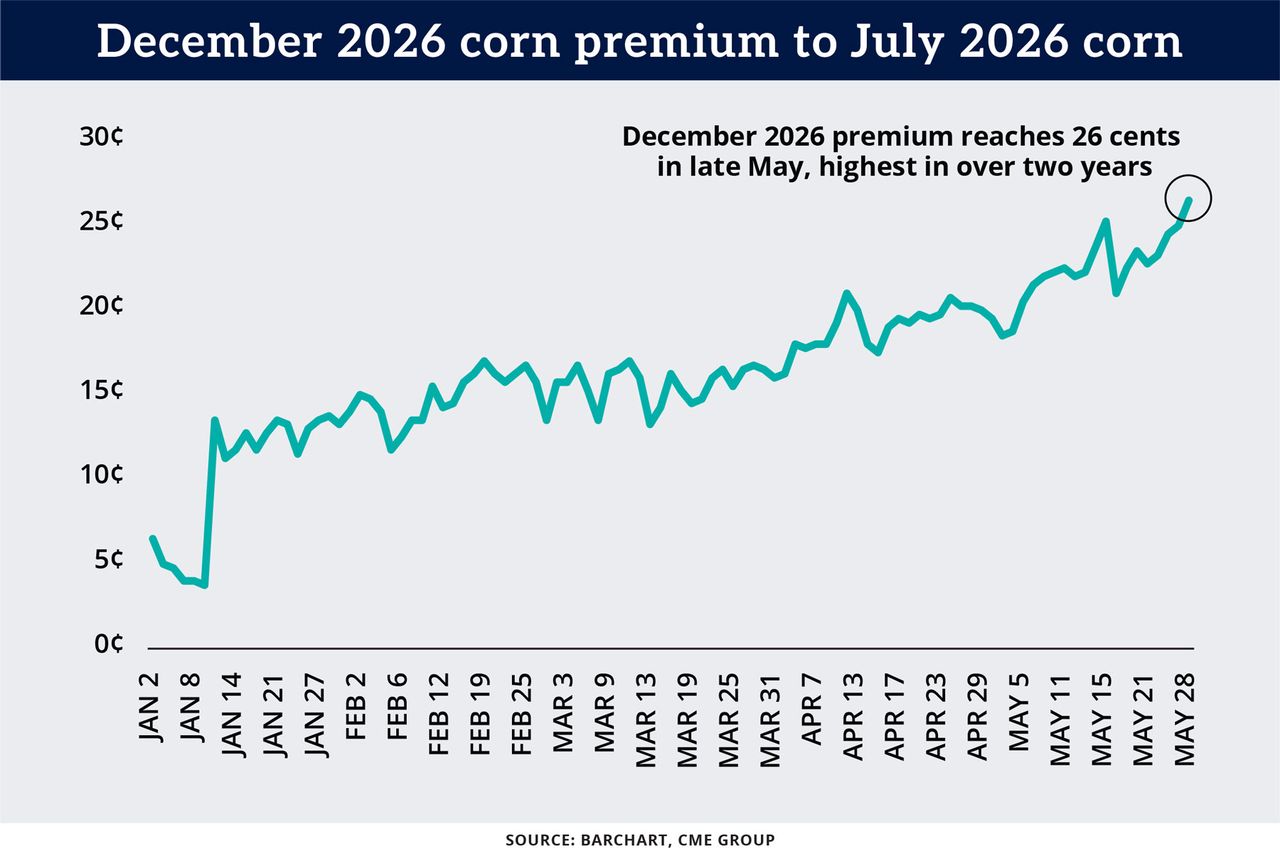

In late May, for example, the December 2026 futures premium to the July contract topped 26 cents, the highest in over two years. While that’s an old-crop vs. new-crop comparison, a similar pattern was developing in new-crop contracts, with the March 2027-December 2026 premium recently nearing 15 cents, nearly double levels from mid-March.

This was happening even as the corn market went into a late-May nosedive that sent December 2026 futures tumbling from a 2½-year high around $5.06 per bushel.

Such carry patterns aren’t unusual. Last year produced similar behavior, as premiums climbed from spring lows and expanded through much of summer. (In 2025, the December-July spread jumped from minus 34 cents to over 14 cents by late June.)

For farmers, it’s worth keeping an eye on shifting carry patterns and other market dynamics to inform hedging strategies and identify possible pricing opportunities, and to get a sense of how the trade views supply and demand fundamentals.

Why is corn’s carry carrying on?

Here are a few factors supporting carry:

Current stockpiles are ample. With the U.S. just off a record 17 billion-bushel harvest, buyers have little concern over whether they can secure sufficient supplies. USDA pegs stocks at the end of the 2025-26 marketing year at 2.14 billion bushels, a seven-year high. That’s keeping near-term prices under pressure.

Acreage skepticism. Many analysts believe USDA’s unexpectedly high Prospective Plantings estimate of 95.3 million acres will be revised lower, perhaps by 1 million acres or more. War-related disruptions that sent fertilizer prices soaring may have prompted some farmers to flip acres from corn to beans. Watch for USDA’s updated planting figures in its June 30 Acreage report.

Biofuels bullishness. Strong demand for ethanol and other biofuels continues to provide long-term ballast for corn and soybean markets, and as long as oil prices stay elevated, some traders will find reasons to buy (or at least not sell heavily).

Weather risks. Planting season was completed at a historically brisk pace, but the bulk of the growing season lies ahead, and with it the frequent concerns over drought or other adverse weather.

The second two factors combined helped December 2026 futures and other “deferred” contracts keep pace with nearby July futures during a mid-April through mid-May rally. Then, in the subsequent sell-off, December futures didn’t fall quite as hard as July futures did. And while December futures’ $5-plus foray was fairly brief (about six days), March and May contracts for 2027 remained above $5 into early June.

How to proceed?

In carry markets, some advisers recommend options-based strategies to “capture the carry” — i.e., selling call options on deferred futures at levels above current prices — but other factors should be carefully considered, including storage costs and tolerance for risk.

Also, remember a strengthening carry doesn’t mean farmers should sit on last fall’s or this fall’s harvest and wait till the new year to sell. Positive carry is no guarantee of higher prices later, and such premiums tend to disappear as the year moves along.