U.S. wheat producers are dealing with what seems like more than their fair share of short hands in recent years, including drought, weak grain prices and stiff export competition, and sometimes all of the above all at once.

Add another item to the list: Americans are consuming less flour-based food.

In the first quarter of 2026, wheat ground for flour in the U.S. totaled 222.4 million bushels, down 2% from the same period in 2025, according to a recent USDA Flour Milling report. That marked an acceleration of a 1.3% year-over-year decline in the fourth quarter of 2025, which came despite a larger harvest.

As the milling rate slowed, daily flour milling capacity tumbled 9.2% in the quarter to 1.458 million hundredweight (145.8 billion pounds), the lowest since USDA began collecting data in 2015, CoBank analysts wrote in a recent report. All flour production dropped 10.4% to 94.6 million hundredweight.

The reasons, or culprits, depending on your perspective: Americans’ accelerating dietary shifts toward animal-based protein, as well as the availability of GLP-1 weight-loss supplements designed to reduce a user’s appetite, CoBank said.

“Consumer demand for protein is taking its toll on wheat-based consumer products and flour milling,” said Tanner Ehmke, CoBank lead economist for grain and oilseeds. “The continual fall in flour milling rates ties directly to falling bakery sales at grocery stores, particularly for desserts, sweet goods and breakfast items like muffins and bagels, as consumers shift to protein-based items like eggs and sausage.”

Demand meets drought

While demand is dropping price opportunities for farmers, drought is also curbing how much wheat they have to sell.

Prices impacted by eroding consumer demand comes at a particularly inopportune time for hard red winter wheat producers in the early stages of a harvest that was hit hard by Southern Plains drought. The soft red winter crop is in better shape, thanks to ample rains in the prime growing areas of the eastern and southern Midwest.

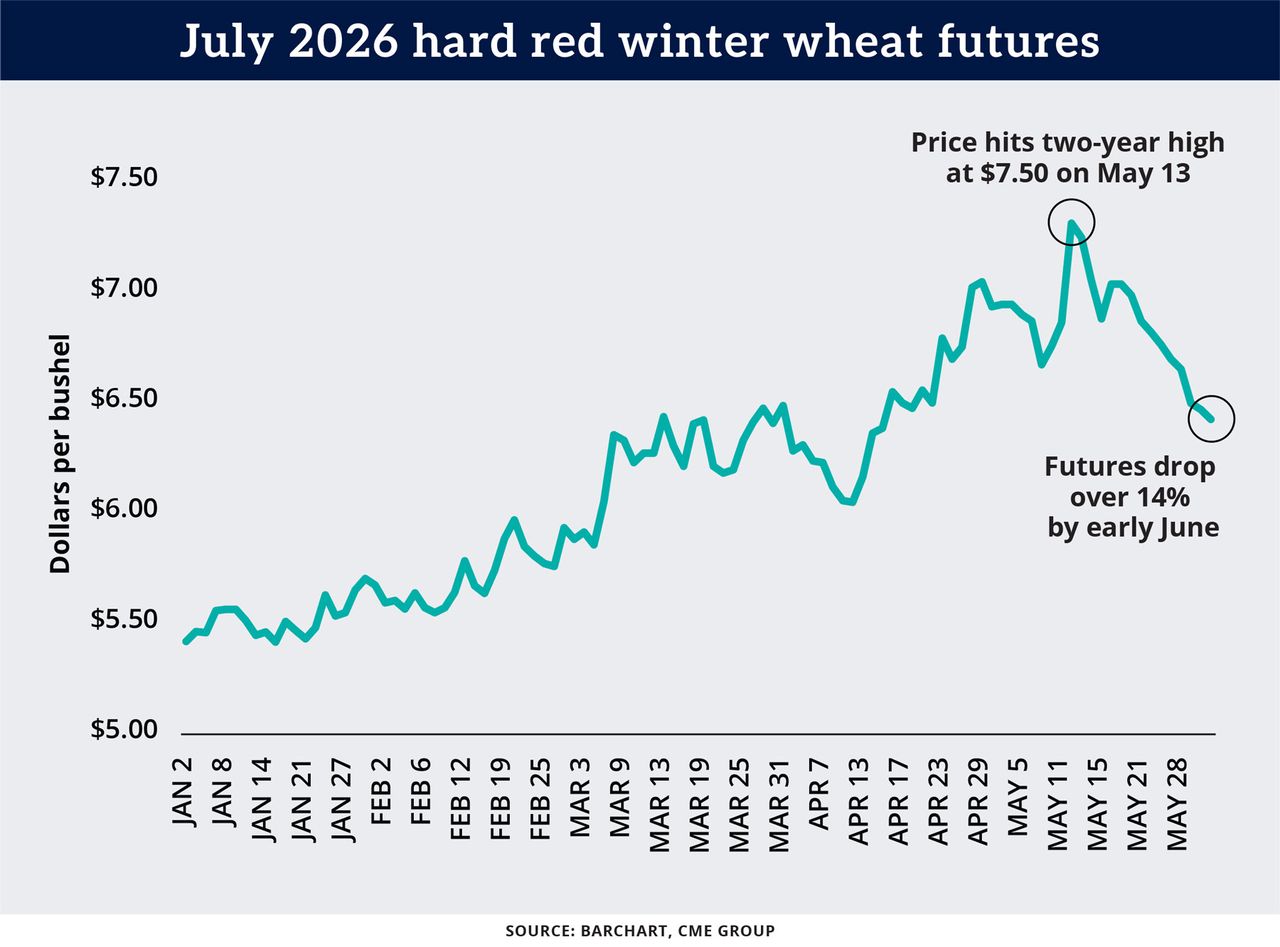

Overall, the 2026-27 U.S. winter wheat crop is expected to shrink 25% to 1.048 million bushels, the smallest since 1965, based on a USDA report last month. While traders might expect a short crop to raise prices, that’s not what’s happening in wheat. The wheat market has given back most of this spring’s brief drought- and war-driven rally.

As of the beginning of June, July HRW futures had tumbled over $1, or more than 14% from a two-year high at $7.50 per bushel reached in mid-May. Wheat rallies do tend to be short-lived, in part because of an abundance of cheaper competing supplies from top producers like Russia on the global export markets. Slumping corn prices also is scaring buyers away.

Hope is in the carry

Markets heading one way in a hurry can, and eventually do, shift back in the other direction, and this one shows some glimmers of longer-term hope for higher prices. USDA forecasts U.S. wheat stockpiles will contract 19% by the end of the 2026-27 crop year. The shrinking supply outlook is fueling an expanding market “carry,” referring to the premium deferred futures contracts hold over nearer-term counterparts.

For example, the premium May 2027 HRW futures held over the July 2026 contract recently neared 50 cents, the highest since mid-April. HRW futures for July 2027 forward were trading above $7. On the surface, a carry market suggests it may make sense to store grain and sell it later, and some advisers recommend options-based strategies to “capture the carry.” But other factors should be considered, including storage costs and risk tolerance.

In addition to carry trends, a few other things to keep an eye on include early results from the winter wheat harvest and USDA Crop Production reports June 11 and July 10. Might USDA revise its harvest figure higher, or could it shrink further? Markets will be watching closely.