USDA’s monthly World Agricultural Supply and Demand Estimates are often dismissed as light-hitting afterthoughts compared to the power-hitting Acreage and Crop Production reports. But when your market is full of rampaging bears swinging Thor’s hammer, everything looks like a nail.

That’s basically what happened when USDA’s June WASDE took a swing at the corn market. The report offered only small adjustments to the U.S. balance sheet for corn but also sizable upward revisions to South America’s production, plus a surprise “spoiler” appearance: India.

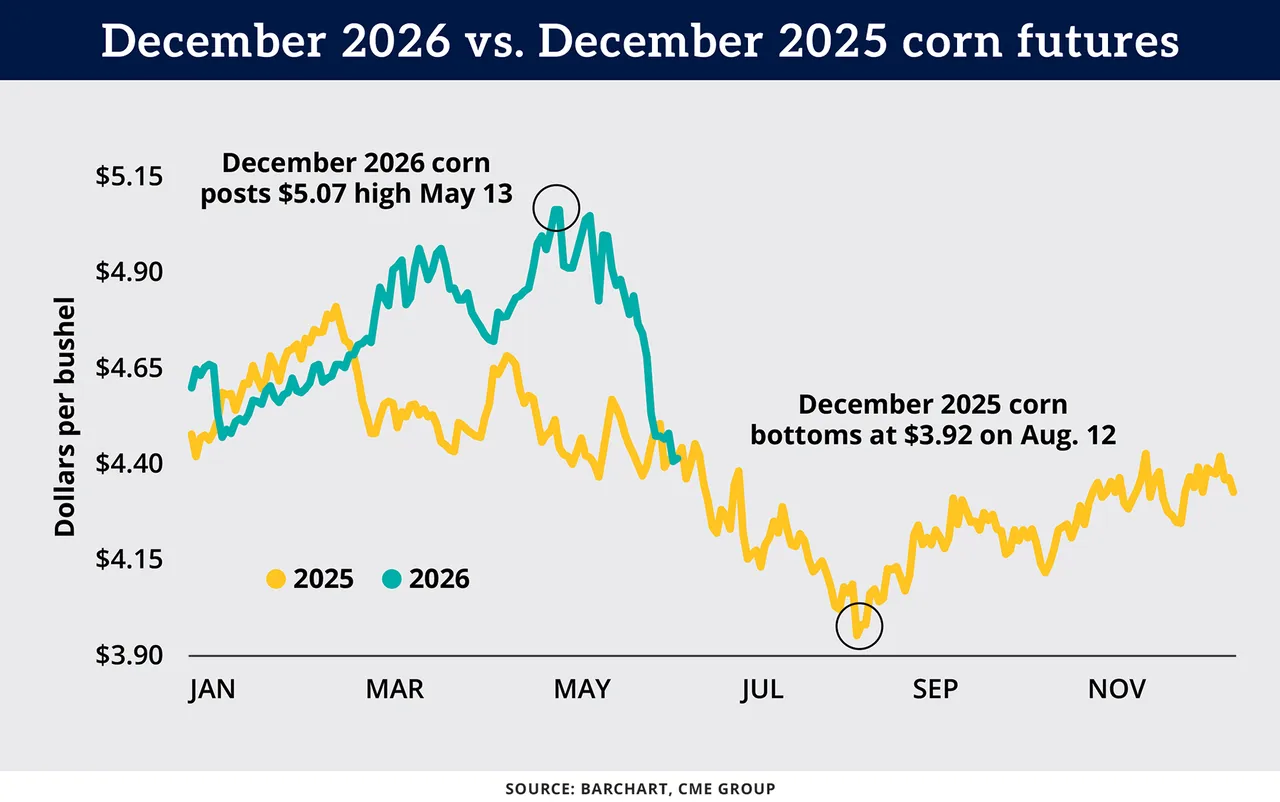

The bigger global numbers combined with bearish Midwest weather were enough to keep corn futures in a tailspin, with the new-crop December price tumbling to a contract low near $4.35 per bushel a day after the report. December futures plunged a stunning 13% by mid-June from a mid-May high around $5.07.

Troublesome questions are surely swimming through farmer minds: How much lower can prices go? Are we anywhere near a bottom? First, a few takeaways from the June WASDE:

U.S. is well-supplied. USDA raised estimated corn stockpiles at the end of the 2025-26 marketing year by 3 million bushels to 2.15 billion bushels, a seven-year high. That also bumped 2026-27 ending stocks up 3 million bushels to 1.96 billion bushels.

Exports remain red-hot, ethanol a little cooler. USDA raised 2025-26 exports an additional 25 million bushels to a record 3.33 billion bushels, the fifth increase of the year. USDA also lowered ethanol use by the same amount, dropping it to 5.58 billion bushels.

India provides global supply boost. USDA hiked Brazil’s corn harvest 3 million metric tons, or 2.2%, to a record 139 MMT (5.47 billion bushels), and boosted Argentina’s crop 2 MMT to 61 MMT. Those increases weren’t really surprising. What did catch the grain trade off guard was the “discovery,” as analysts put it, of about 9 MMT of production from India. Altogether, this added about 14 MMT (551 million bushels) of “found” supplies and gave a 2.2% boost to 2025-26 global ending stocks.

The quick takeaway: The world has plenty of corn, for now. No shortages and, for speculators, really no reason to be long in corn. (Managed funds, in fact, flipped to a net-short position a few days before the report after holding a hefty net-long position for the previous three months, based on Commodity Futures Trading Commission data.)

For farmers who have priced little or none of their expected harvest, the market’s recent behavior poses an obvious conundrum. Sell at depressed levels, lest prices nosedive even more? Or hope a bottom will form soon, and USDA’s June 30 Acreage report or a weather scare will deliver a bullish shot in the arm? Some advisers suggest a “go-slow” mindset, noting the potential for summer weather scares to fuel a rally.

However, recent market history isn’t particularly encouraging.

On June 11, 2025, a year before the latest WASDE release, December 2025 corn closed at about $4.40, almost exactly the same price where December 2026 corn settled post-report. By mid-August 2025, as the trade grew increasingly confident a potential record harvest was in the works, December 2025 corn tumbled to $3.92, an 11% drop.

But prices quickly bounced back and the market spent only about a week trading below $4 last year. Sub-$4 visits were relatively brief thanks to strong demand. Will the buy side come to the rescue again in 2026? Perhaps. But prepare for more downside in the meantime.