The Pilgrims didn’t serve Tofurky with soybean stuffing at the first Thanksgiving – at least, not that we know of. Corn, by contrast, has long ties to the feast. But traders looking for holiday profits might consider going light on the maize.

Over the past five decades nearby corn futures tended to lag behind the oilseed after Thanksgiving, a trend that is even more pronounced in presidential election years like 2024.

For perspective on turkey-day trading (as opposed to day-trading turkeys), I looked at patterns dating back to 1973, when the modern era of futures really began after the “Great Russian Grain Robbery.” Following widespread crop failure Russia purchased massive amounts of grain, deals that went unnoticed by markets because exporters like the U.S. lacked reporting systems. When the news finally broke markets exploded, sending prices to unheard of levels.

Don’t look for a weather rally

Drought in countries of the former Soviet Union, as well as parts of Europe and the Americas, is back in the news. Markets aren’t showing much interest because harvests are still months away and the true extent of damage remains unknown. So, fears about demand fueled by concerns about weakening economies around the world pushed soybeans to new November lows, triggering sell signals from some chart-based “technical” trading systems.

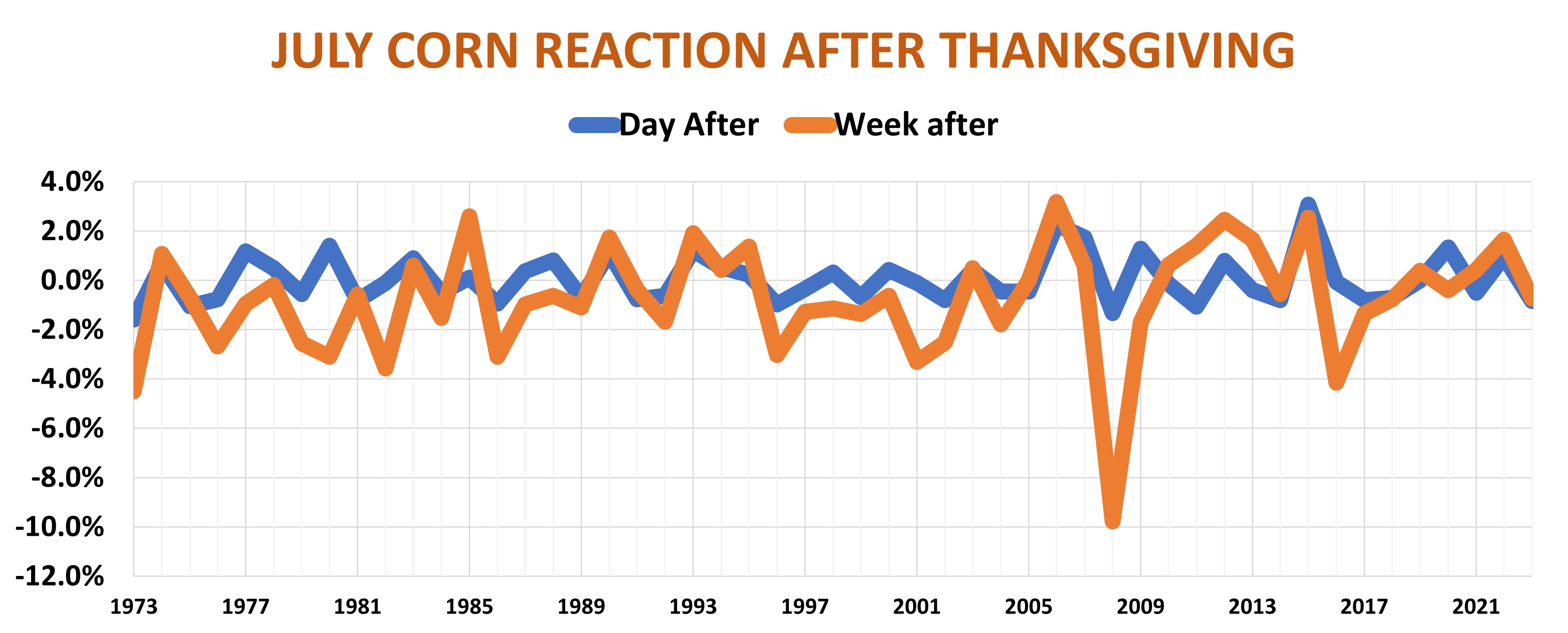

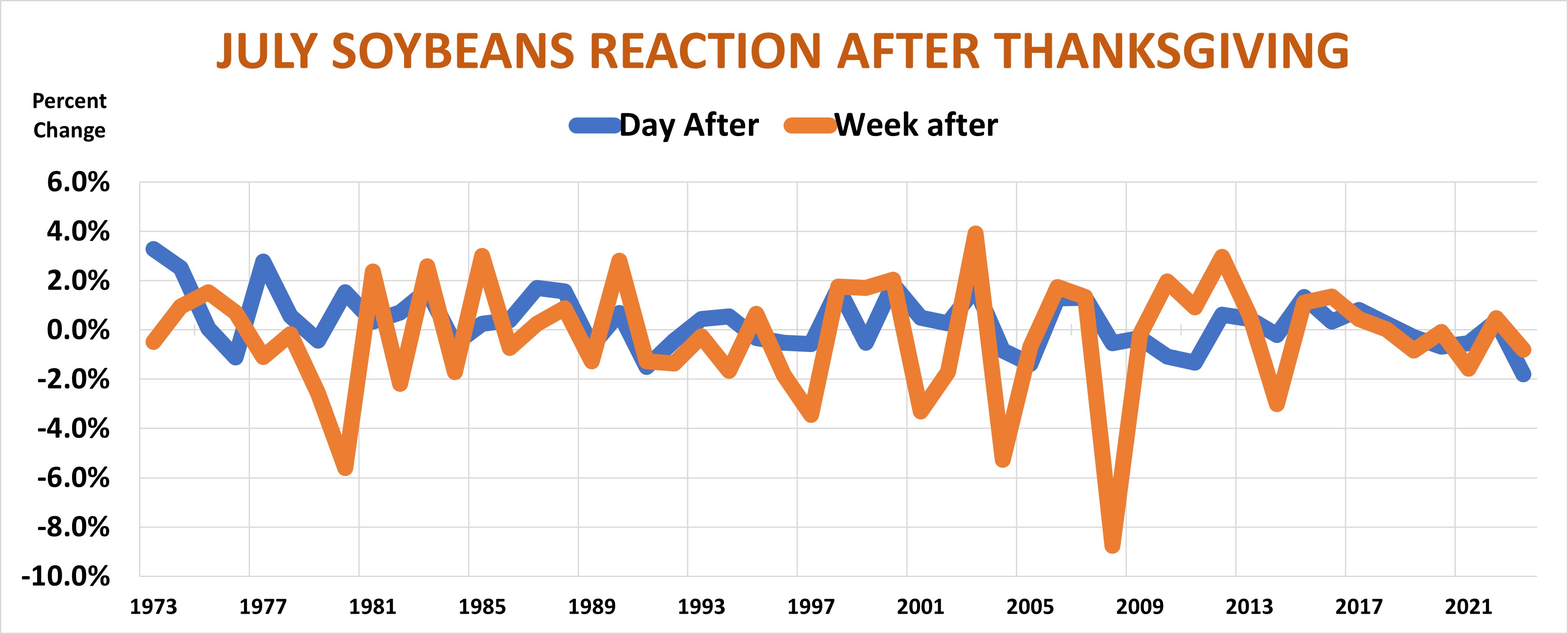

Holidays sometimes disrupt even the most orderly markets: While the cat’s away, the mice will play, so to speak, and thin volumes can exaggerate price swings, triggering stop orders that only exacerbate volatility. As a result, Black Friday markdowns aren’t only for big box stores. Christmas shopping patterns also can set the tone for retail sales into the end of the year and beyond, so we looked at corn and soybean futures moves one day and one week after Thursday spreads become leftovers.

Beware big days

Black Friday isn’t a total bust for corn. Futures on average on the day after the holiday gained about a half-cent since 1973.

But a few big doorbuster days with double digit gains, such as 2015, skew the average a bit because the number of Black Fridays with losses outnumbered those with gains. Futures ended the day higher only 43% of the time. One week after the holiday futures lost an average of around 2 cents a bushel, finishing with gains just 35% of the 51 years.

Nearby soybeans also posted average gains the day after Thanksgiving with losses one week later, around two cents up and down respectively. But gains prevailed 59% of the years the day after the holiday, with futures higher a week later nearly half the time.

Seasonal trends tell story

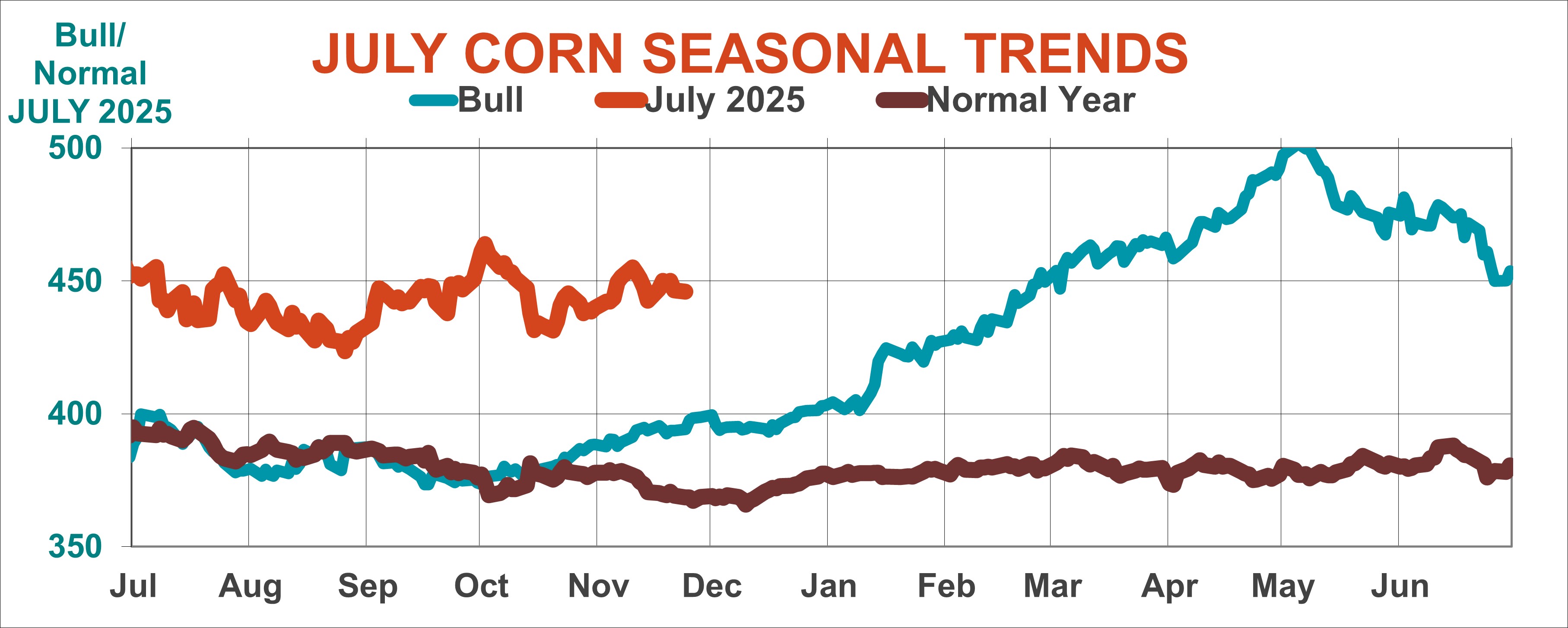

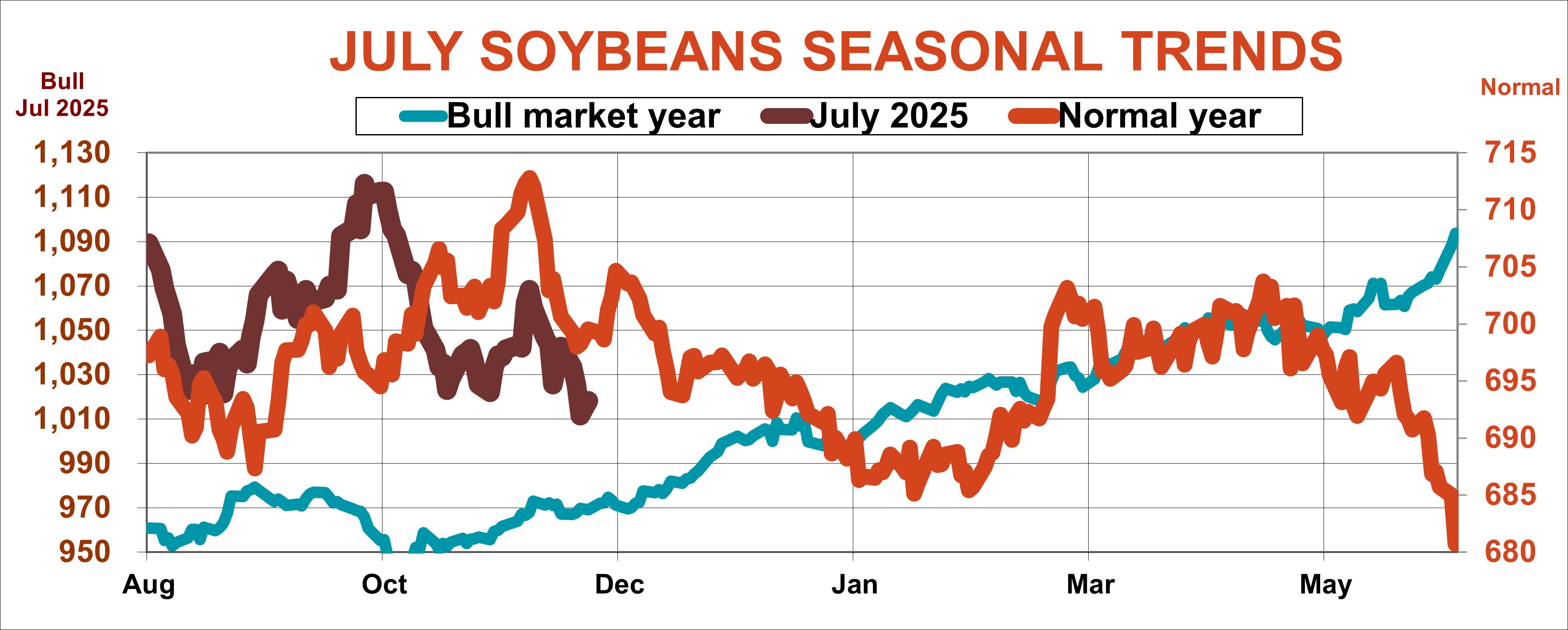

Differences between the two crops also show up on charts of seasonal trends. Those tendencies could be important this time around because both corn and soybeans appear to be following patterns typical for years with normal price movements.

July corn on average trends mostly flat to lower at the end of November, a pattern the contract appears to be settling into this year. July soybeans also are on average lower, consolidating after bottoming just after the midway point. But soybeans get a pop into the start of December.

Two factors could be in play. Weakness in July corn could be influenced by spread trading into the start of deliveries on December futures at the end of November. Most years the market adds carry, widening spreads between December and delivery in July the following summer. This encourages corn to go into storage, which it needs to do because demand is spread out through the year.

Soybeans, by contrast, are in their peak selling season in the month or two after harvest, for better or worse. Prices can go up a lot, posting 40.5-cent gains in 2012. But they can also lose a lot, falling 80 cents in 2008, for example. And while corn can get a “Santa Claus” rally into January, soybeans trend weaker, feeling effects from the start of harvest in South America.

Election years

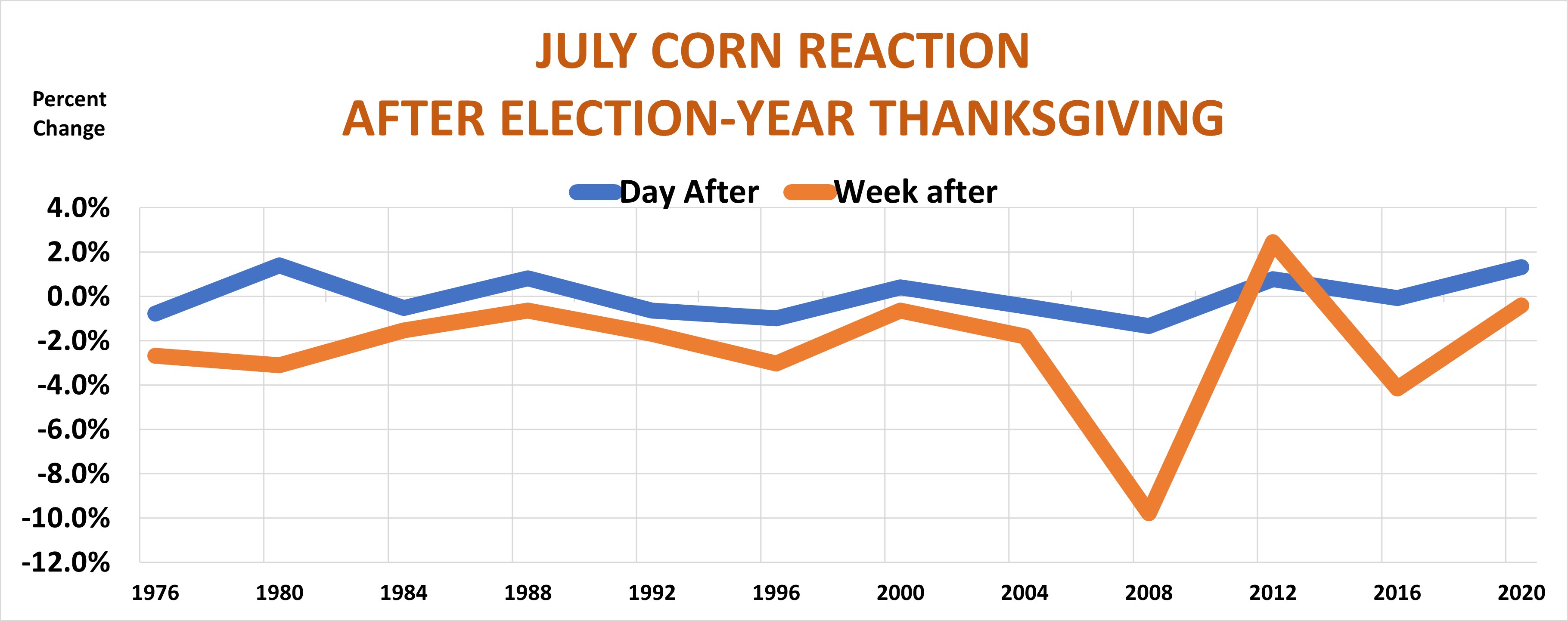

These trends emerge even more clearly when only years with presidential elections are considered. Corn losses the week after Thanksgiving were greater than the day after in each of these dozen quadrennial years. The one exception is 2012, when traders geared up for January production updates following the drought.

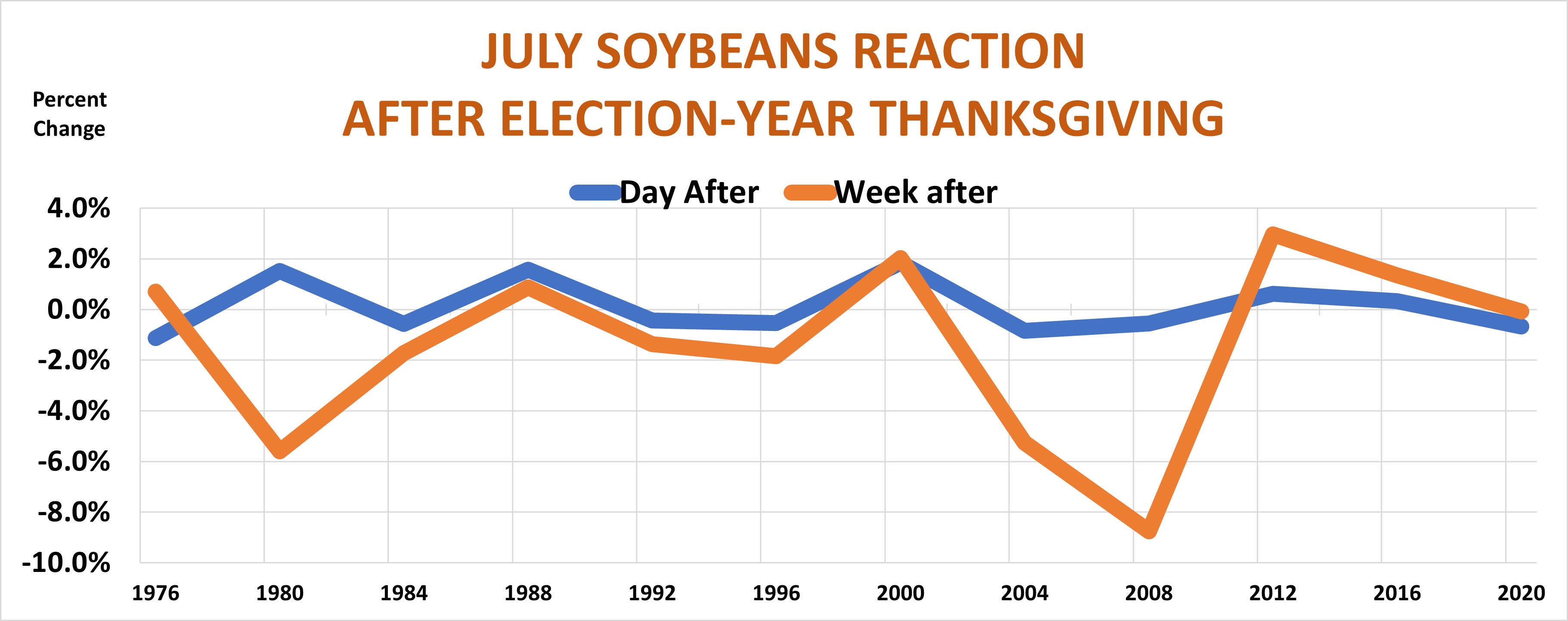

July soybeans also were stronger a week after the vote in 2012, compared to day-after results. That pattern also prevailed in 2016 and 2020, in addition to 1976. This means soybean losses and gains a week after Thanksgiving were less predictable based on day-after finishes. Corn gains and losses tended to move in the same direction, either up or down the day and week following the election, while soybeans could go either way.

What will happen in 2024?

- Worries about tariffs could come into play, particularly for soybeans, but broader market concerns also could have influence.

- The U.S. Department of Labor reports jobs growth Dec. 6.

- The Consumer Price Index is updated Dec. 11.

- The Federal Reserve updates monetary policy Dec. 18. The Fed is likely to shave another one-quarter of 1% off its benchmark for short-term interest rates.

Investor concerns about prospects for a big stock market rally in 2025, or a bust if interest rates stay high and inflation lingers, could spill over to ag markets once again.