Corn futures prices have rallied nearly $1 since September thanks to strong demand and lower than expected U.S. production.

Back in September 2024, U.S. corn ending stocks were pegged at a whopping 2.057 billion bushels. Fast forward five months, and now U.S. corn carryout for 2024-25 is at a much tighter number: 1.54 billion bushels.

What’s happened

A perception of high carryout back in September and harvest pressure weighed on the market, holding corn prices near the $4 price point back in early autumn. End users stepped up quickly and bought on value, pushing export sales and ethanol demand higher.

In recent weeks, corn futures prices continue to swirl near the $5 price handle. While the recent February USDA WASDE report lacked fresh fundamental news, the corn market remains focused on the previous month’s surprisingly bullish January USDA WASDE report, which reduced U.S. corn yield, thus lowering U.S ending stocks for the 2024-25 crop year and dropping corn global carryout as well.

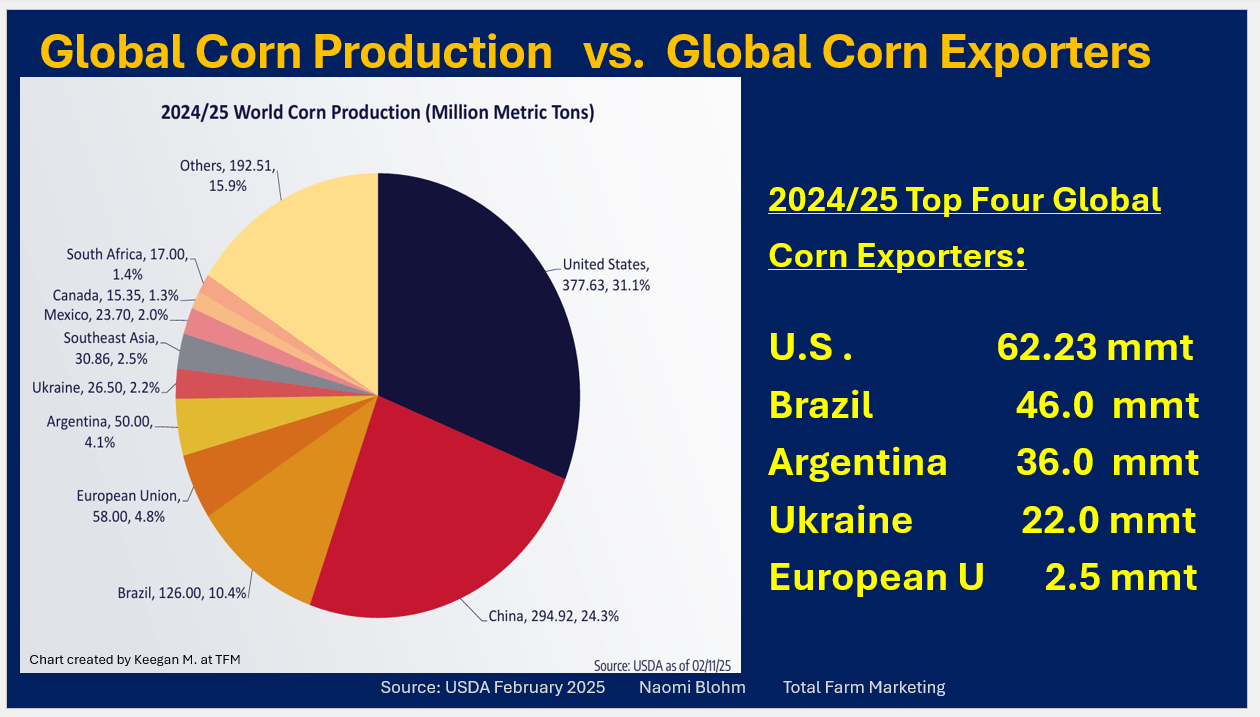

As it sits, from the data in the February 2025 USDA report, U.S. corn carryout is now pegged at 1.54 billion bushels while global corn carryout is pegged at 290.31 mmt (down from 315.81 in the 2023-24 crop year).

At the moment, without fresh friendly fundamental news from the February USDA WASDE report, the path of least resistance for corn futures prices is likely sideways to slightly lower.

Is there anything on the horizon that could inspire a price rally? Potentially yes, with the answer lying in South American corn production.

From a marketing perspective

Looking ahead over the coming weeks, without any additional USDA reports coming up, traders may instead keep an eye on South American weather, and specifically weather in Brazil.

Many questions are beginning to surface regarding second crop corn production in Brazil, otherwise known as the safrinha crop. The safrinha is planted in late February and early March right after the combines harvest soybeans in Brazil, with early corn harvest then beginning in August.

This safrinha corn is the crop that many nations of the world rely on for import during August, when the U.S. crop is not yet ready to be harvested.

The question is, can the Brazil corn crop afford to lose any production? Not really. And that matters to global corn production, global ending stocks, a potential increase in U.S corn export demand and a potential corn price increase down the road.

Over the past decade, Brazilian farmers have taken advantage of their growing seasons and weather and have discovered the benefit of double cropping corn behind soybean planting. Their ability to double crop has created a dramatic increase in their corn production.

Back in 2011, Brazil corn production was near 75 million metric tons. But thanks to double cropping corn, their production ballooned.

Right now, growing in Brazil is first crop corn, which primarily consists of 25% of their total expected production. The USDA currently is estimating Brazil 2024-25 production to be 126 mmt, which means approximately only 32 mmt of corn is growing in their fields right now as “first-crop” corn. That also means that the remaining 94 mmt of expected Brazil corn production is just getting planted.

This “first-crop corn” will be harvested in late February and March and primarily is kept in Brazil for their own domestic use. According to USDA, Brazil domestic consumption is pegged at 87.5 mmt, with 64 mmt of that slated for domestic feed. So that means, what is growing right now in Brazil will likely stay in the country for livestock feed, but then, some of that second crop corn needs to also stay in Brazil to meet further domestic demand as well.

The USDA pegs Brazil exports (which is the bulk of their second-crop corn) at 46 million metric tons. If Brazil exports 46 million metric tons, and they use 87.5 mmt for domestic consumption, then total demand is slated for 133.50 million metric tons.

And yet, according to the USDA, they are expected to only grow 126 mmt, down from the January USDA number of 127 mmt. Hmm.

Looking to Argentina. Yes, we know corn and soybean production has been slightly reduced due to recent dry weather. Last year, Argentina corn production was 50 mmt. This year, the USDA suggests their production capabilities will also be at 50 mmt. But please note, all that corn is spoken for already in terms of demand: 14.3 mmt will be used for domestic needs and 36 mmt will be used for exports. That leaves combined demand at 50.3 mmt, using all their expected production.

Prepare yourself

With corn, if there is a weather issue in Brazil for the safrinha crop, the market may start to trade that news during the months of mid- to late March or April.

Regarding your marketing strategy, if you are choosing to sell corn in your bin sooner than later, perhaps consider a corn re-ownership strategy, just in case weather flares up in Brazil in a few months.

But also keep in mind, that holding out hope for a poor second-corn crop in Brazil is not a great way to market your corn in your bin. What if they end up having “good enough” yields and sufficient production to meet that demand? Be ready for anything.

Reach Naomi Blohm at 800-334-9779, on X: @naomiblohm, and at naomi@totalfarmmarketing.com.

Disclaimer: The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Individuals acting on this information are responsible for their own actions. Commodity trading may not be suitable for all recipients of this report. Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. Examples of seasonal price moves or extreme market conditions are not meant to imply that such moves or conditions are common occurrences or likely to occur. Futures prices have already factored in the seasonal aspects of supply and demand. No representation is being made that scenario planning, strategy or discipline will guarantee success or profits. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing. Total Farm Marketing and TFM refer to Stewart-Peterson Group Inc., Stewart-Peterson Inc., and SP Risk Services LLC. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services, LLC is an insurance agency and an equal opportunity provider. Stewart-Peterson Inc. is a publishing company. A customer may have relationships with all three companies. SP Risk Services LLC and Stewart-Peterson Inc. are wholly owned by Stewart-Peterson Group Inc. unless otherwise noted, services referenced are services of Stewart-Peterson Group Inc. Presented for solicitation.