USDA’s annual June Acreage and quarterly Grain Stocks reports approached with at least a little more buildup and drama this year, given recent global upheaval, and brought the usual report-day price volatility.

When all was said and done, one word might sum up farmer reaction: relief. As in, relief that the numbers didn’t drive corn prices even lower after a month-and-a-half downdraft.

Even as the reports — among the most market-moving USDA data sets of the year — threw off a mix of bearish and bullish signals, the bulls seized the initial advantage as December corn futures bounced back from a contract low and showed signs of resurgence in early July. Here are a few takeaways:

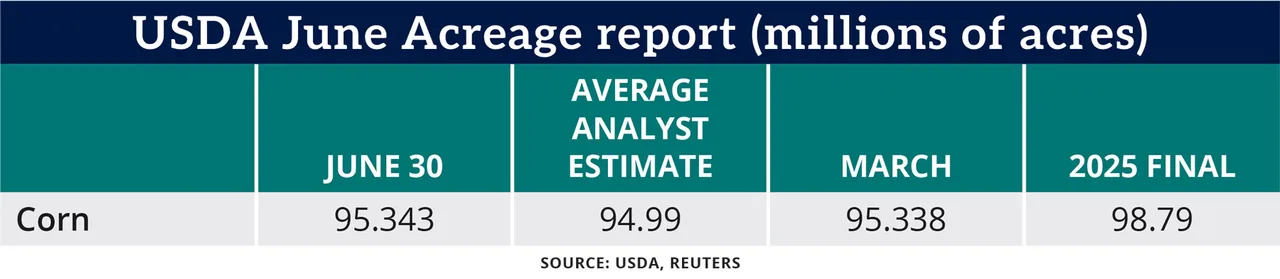

No big acreage switch. USDA raised its 2026 U.S. corn plantings estimate to slightly over 95.34 million acres, up about 5,000 acres from its March Prospective Plantings forecast and contrary to expectations for a cut of about 346,000 acres. Plantings are down 3.5% from a nine-decade high of 98.8 million acres in 2025 but would still be the fourth highest since 1944.

Shorter mountains of corn. USDA reported nationwide corn stockpiles as of June 1 at almost 5.3 billion bushels, up 14% from the same date a year earlier but about 113 million bushels under the average trade estimate and below even the lowest trade guess. On-farm stocks as of June 1 totaled 2.96 billion bushels, up nearly 16%. Presumably, some of that corn has been sold and hauled away by now, but the numbers suggested farmers still had piles of unsold inventory late in the crop year.

Corn’s less-shiny crown. USDA estimated acreage declines in 10 of 11 top corn states in the Midwest and Plains, with Iowa plantings contracting 550,000 acres, or 4.1%, to 13 million acres. One exception: Corn area in Kansas is up 200,000 acres to 7.05 million acres.

The slight boost in corn acres contrasted with speculation earlier this spring that disruptions to global fertilizer and fuel markets would lead to a sharp shift away from the grain. Instead, farmers appear to have largely avoided a major switch, possibly because many secured fertilizer before the war broke out.

“It’s apparent that higher input costs due to the Iran war were negligible,” because corn prices pushed up during that acreage decision time and many farmers booked inputs at pre-war prices, said Jeremy McCann, farmer relations manager at Farmer’s Keeper.

At the same time, the quarterly stocks figure tamped down a bearish response to the acreage number, illustrating how strong demand is helping soak up last year’s record harvest while also fueling speculation that USDA may have overstated 2025 production numbers.

The June acreage and stocks figures are always important for recalibrating farmer and trader expectations for existing and impending supplies. But the market, as it does every year, has already moved on to weather, which will be the key price influencer the next month or so. The Midwest was in the clenches of a heat wave in early July, but extended forecasts suggested temperatures would moderate somewhat before the critical pollination phase begins in earnest.

Assuming the crop navigates pollination with little trouble, don’t be surprised if corn prices resume a downward path. (December corn dropped to a contract low around $4.26 on June 30 but bounced back to the low $4.40s before the July 4 weekend.)

“USDA didn’t overwhelm with bearish data,” said Jason Gehler, senior market strategist at Blue Line Futures. “Ultimately, the USDA numbers won’t shift the landscape, leaving weather the main driver for grain and oilseed prices, which currently don’t reflect much risk. Expect corn to drift lower until we get to typical timeframe in early August where we likely set a major seasonal low. Strong demand will spark higher prices later.”