As we move toward harvest, optimism is mounting within the corn market. Industry chatter points to a projected U.S. corn yield significantly above the long-term trend, supported by recent weather patterns reminiscent of historic wet spells. In fact, this July may rank as the wettest for the Corn Belt since 1993, with more precipitation expected this month.

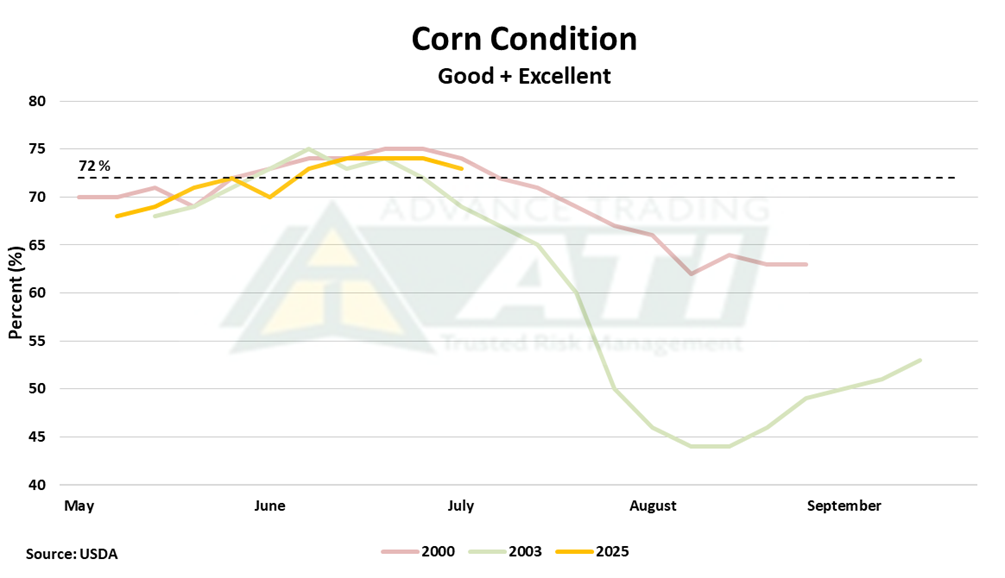

Trade estimates now peg national corn yield in the mid-180s bushels per acre range, a level that, if realized, would set a new all-time record for the United States. This is echoed by recent USDA projections. Market watchers now figure USDA’s July estimate of 181 bpa was cautious. Crucially, the portion of the crop rated as “good” to “excellent” in late July stayed above 72%—a rare occurrence that has happened only five times in previous decades. Such high ratings at this point in the season typically foreshadow strong final yields, provided weather cooperates through harvest.

Historical lessons focus on weather

The story of corn yields is tied to in-season weather. The years 2000 and 2003 serve as stark reminders: both began with optimism, only to experience deteriorating weather, a shift that slashed crop ratings and ultimately cut yields. In both years, despite high early-season ratings, adverse summer weather caused measurable declines in crop potential by harvest.

- 2003. Long stretches of heat and very little rain in July and August caused drought across Iowa, Illinois and Indiana, hurting yields during key growth stages.

- 2000. Early summer was wet, but late July through August saw the return of intense heat—often exceeding 95°F—paired with declining rainfall.

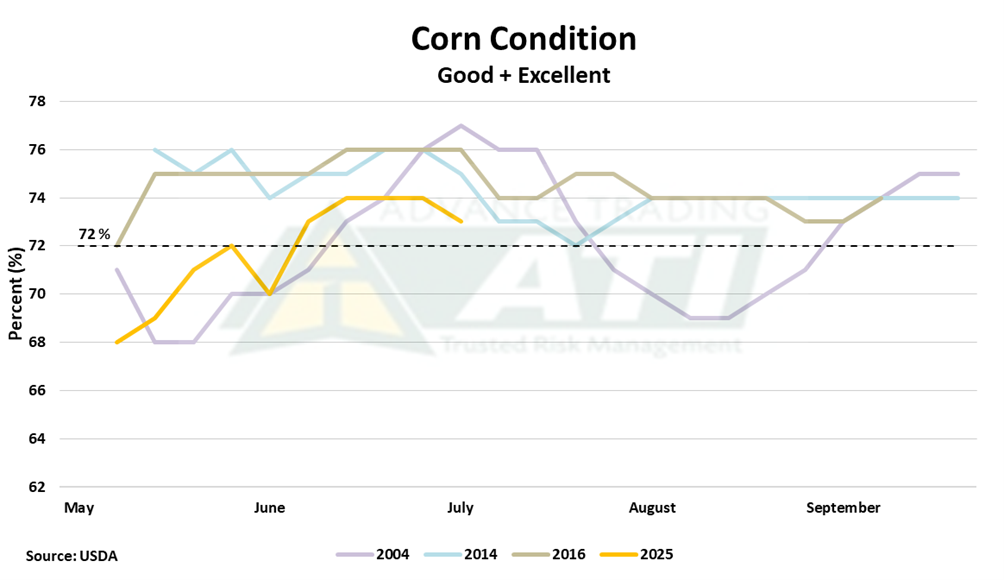

On the other hand, years with steady, mild weather—like 2004, 2014 and 2016—let high “good” and “excellent” ratings persist through the summer, resulting in harvests significantly above the average yield trend.

Market reactions and USDA outlook

Traders have taken note of the supportive weather and robust crop conditions, positioning themselves accordingly in the market. Much like last year, the market appears to have formed its major harvest expectations in July. December 2025 corn futures slid about 15 cents during the month, closing at 411 cents per bushel on July 29, almost identical to the previous year’s price trajectory, with December 2024 futures at 412.2 cents on the same date.

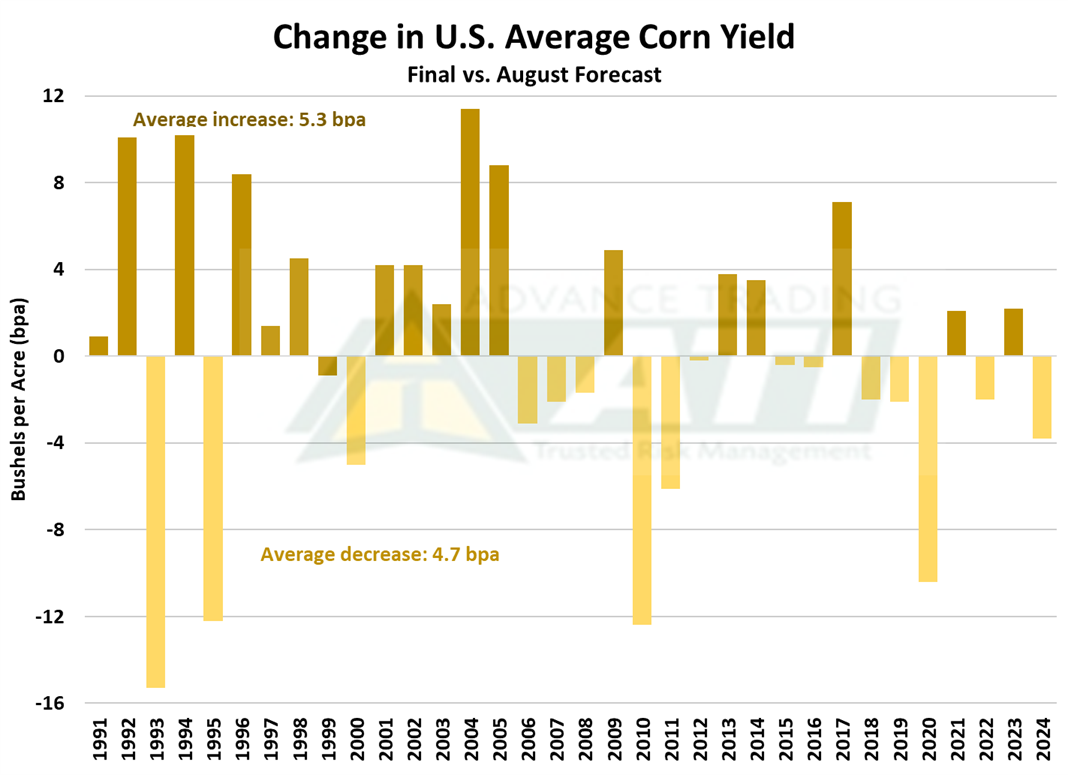

Attention is now sharply focused on the upcoming WASDE and crop production reports, set for release Aug. 12. These reports are widely recognized as major drivers for yield adjustments with an average increase of 5.3 bpa while an average decrease of 4.7 bpa. The USDA’s current “cautious” projection of 181 bpa is expected by many analysts to be revised upward, reflecting the strong crop development and supportive weather so far this season.

The bottom line: Weather will decide

For now, the outlook remains bright, with the Corn Belt’s weather patterns and crop conditions indicating exceptional yield potential. However, if history is any guide, August weather will write the final chapter—prolonged heat or dry spells could still trim yields, as seen in the cautionary years of 2000 and 2003.

Until then, growers and market participants are watching the skies. With favorable forecasts holding, 2025 stands poised to deliver a record-setting corn harvest.

Advance Trading, ATI, and ATI ProMedia are DBAs of CIH Trading, LLC, a CFTC registered Introducing Broker and NFA Member. The risk of trading futures and options can be substantial. All information, publications, and material used and distributed by Advance Trading shall be construed as a solicitation. ATI does not maintain an independent research department as defined in CFTC Regulation 1.71. Information obtained from third-party sources is believed to be reliable, but its accuracy is not guaranteed by Advance Trading. Past performance is not necessarily indicative of future results.