Before the shock of today’s WASDE and crop production reports fully wears off for many, the market is reacting. Here’s what we’re seeing today:

Corn

Bearish. USDA estimated average yield at 188.8 bushels per acre, 4½ bushels above the trade average and nearly 8 bushels higher than the July estimate.

This boosted production to 1.037 billion bushels higher than last month’s estimate. A lot more corn was planted than had been expected, with acreage up 2.4 million from the July estimate and the harvested total 2.1 million bushels higher at 97 million bushels.

USDA increased ending corn stocks for 2025-26 by 457 million, bringing it up to 2.117 bbu.

2024-25 carry-out was reduced 35 million bushels from July, bringing it down to 1.305 billion. USDA’s number factors a 70 mbu increase in exports to 2.820 billion and a 35 million reduction in FSI/ethanol use.

Old crop prices remain forecast at $4.30. The USDA 2025-26 estimate dropped $.30 to $3.90.

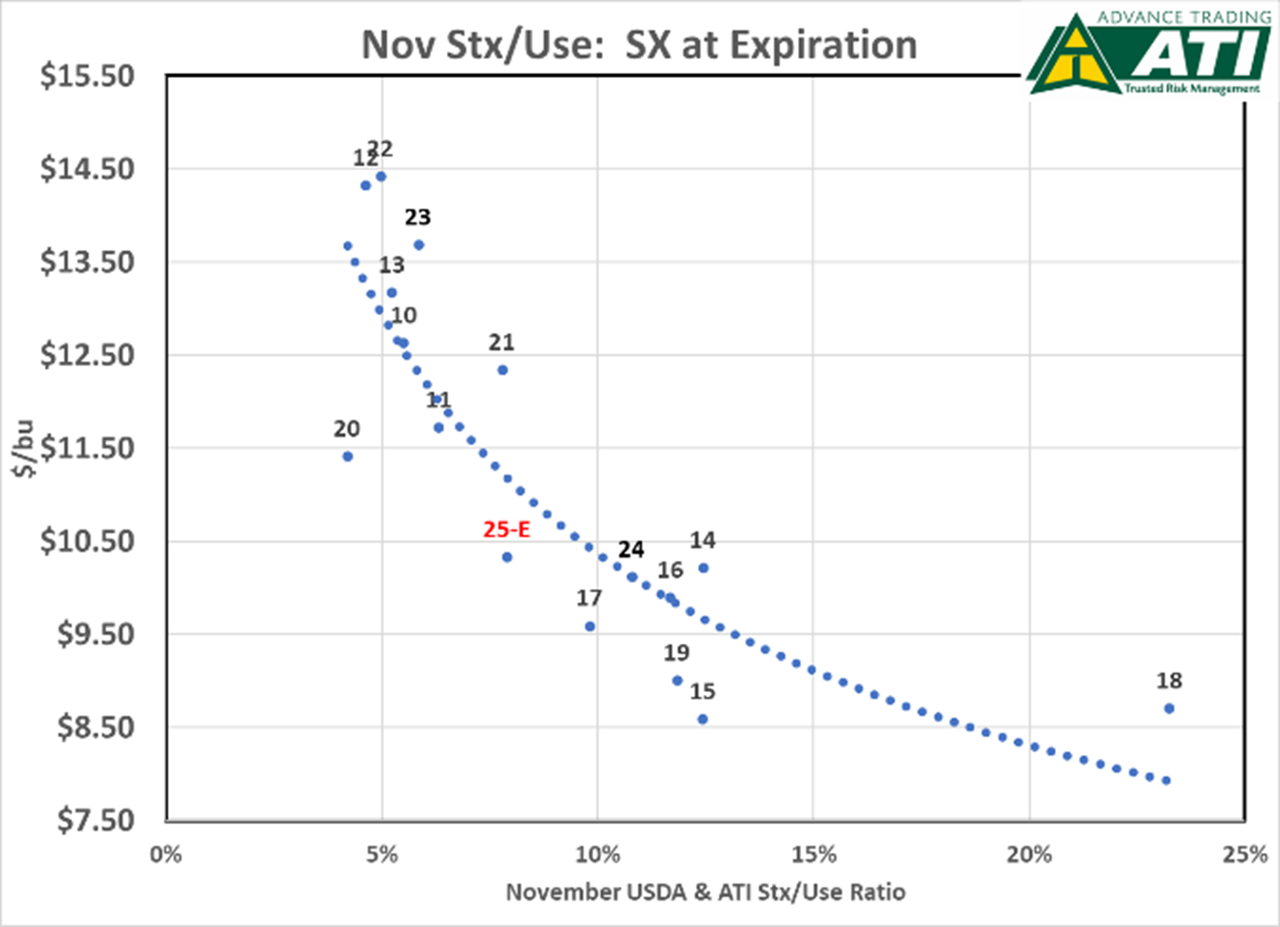

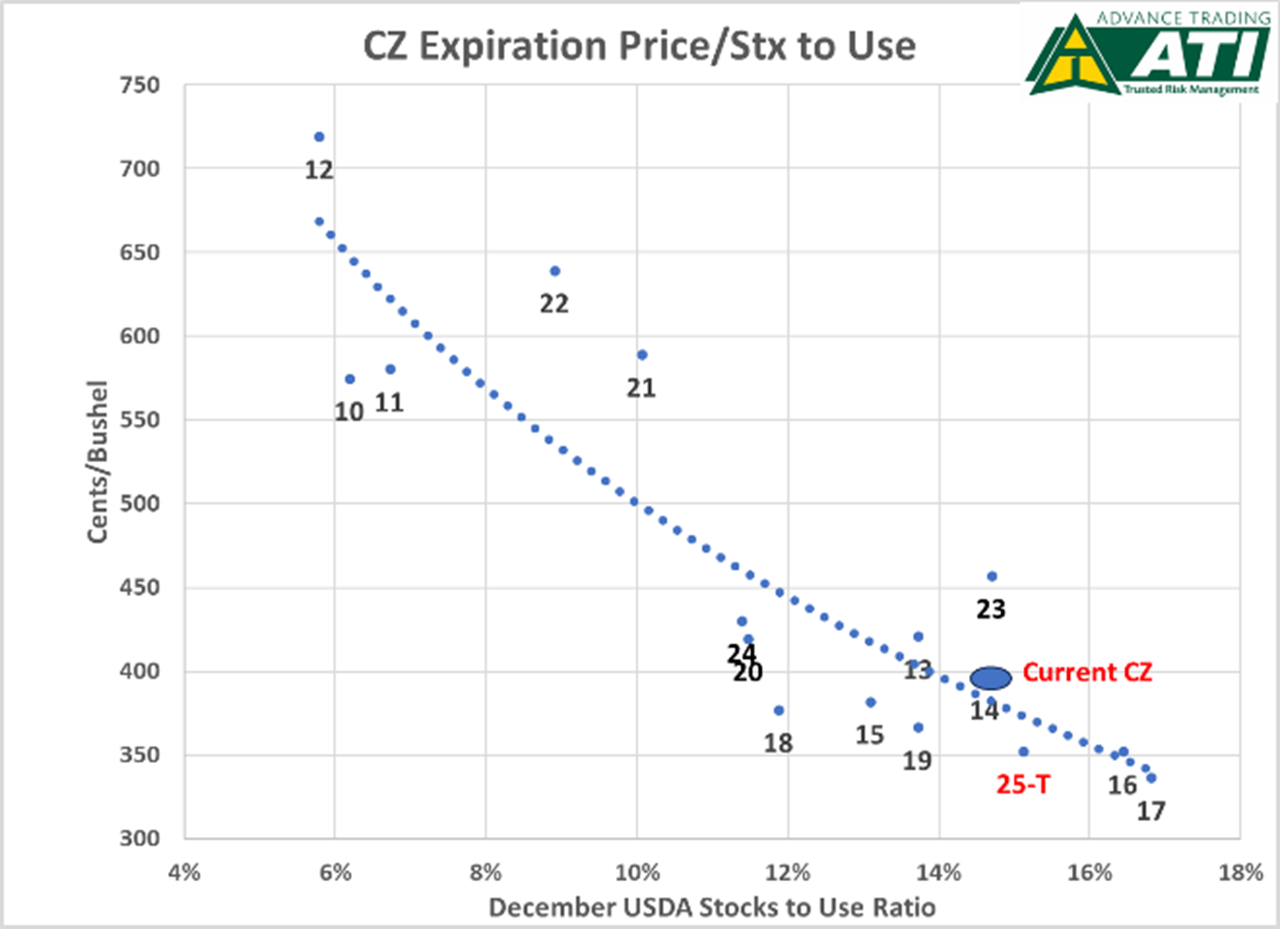

The new crop stocks to ratio jumped from 10.8% to 13.3% this month. The CZ and SX futures graphs below reflect the corresponding historical expiration prices and stocks-to-use ratios along with where the market is currently. CZ at $3.95 would seem to have substantially limited downside. Let’s see how the remainder of the month finishes the crop.

Soybeans

Initially bearish. The SX forecast is a little below “trend” and could be approaching that “explosive territory” were it not for expectations of another record South American soybean crop.

SX lost 15 cents out of the gate and then bounced back up 30 cents. Main driver in the market’s ultimate reaction was a 3.5 million acre drop in acreage planted, from 83.4 to 80.9 million acres. The harvested total went down 2.4 million acres to 80.1 million acres.

USDA raised its average yield forecast 1.1 bushels to 53.6 bpa, nearly 3 bpa above last year.

Old crop carry-out was reduced 20 million bushes to 330 mbu on 10 higher estimates for both crush and exports, with ending inventories 19 million bushels less than trade expectations.

The net of acreage and yield reduced the new crop supply by 63 mbu.

Exports in the coming year were trimmed 40 mbu to 1.705 billion. 2025-26 ending stocks were down 20 million from last month to 290 mbu, or 68 mbu below the trade average.

Questions remain on final yield as the market moves into the last half of August, which explains the supportive price action seen in soybeans today.

The other large question looming over the market is: Will we see a U.S./China trade deal that stimulates some soybean buying? Recall that China imported over 825 mbu of U.S. soybeans in 2024-25 with nearly 470 mbu of that total occurring during the first quarter.

China is believed to be 100% covered by Brazil for its September needs and October is likely more than 50% booked. And expectation is that South America will September 2025 with more soybeans on hand than last year – at least 400 mbu more than last year. It remains to be seen whether this amount of supply can cover virtually all of China’s SON import requirements. But it could be close.

Wheat

Neutral. However, sharp declines in corn are weighing on winter wheat classes.

The updated survey-based estimate of U.S. other spring production of 0.484 bbu was below the average trade estimate of 0.497 bbu.

HRS production is estimated at 0.449 bbu, which is nearly 19 mbu (4%) lower than the July projection.

Winter wheat production was estimated at 1.355 bbu compared to the average trade guess of 1.344 and up 10 mbu (1%) from last month.

The largest increase relative to July was seen in HRW: up 15 mbu (2%) to 0.769, while SRW was up 3 mbu (1%).

All wheat exports were increased by 25 mbu reflecting the brisk pace of HRW sales and shipments.

U.S. ending stocks were reduced by 21 mbu to 0.869, which was below the average trade estimate of 0.882.

No changes in exports from major competitors.

The collapse in corn prices could continue to weigh on HRW and SRW, while attention now shifts to production prospects in Australia and Argentina.

Advance Trading, ATI, and ATI ProMedia are DBAs of CIH Trading, LLC, a CFTC registered Introducing Broker and NFA Member. The risk of trading futures and options can be substantial. All information, publications, and material used and distributed by Advance Trading shall be construed as a solicitation. ATI does not maintain an independent research department as defined in CFTC Regulation 1.71. Information obtained from third-party sources is believed to be reliable, but its accuracy is not guaranteed by Advance Trading. Past performance is not necessarily indicative of future results.