Hopes for a rebound in soybean prices likely depend on the world’s largest oilseed importer. So, let’s look at the export picture, and China specifically.

Though China’s purchases continued to improve in July, rising 9.4% above year-ago levels, the third straight monthly increase, U.S. sales have yet to join the party.

- U.S. shipments from the 2024-25 crop remain 6.2% lower as the end of the marketing year nears.

- China has yet to book any new crop from the U.S. Why bother as end users chew through another big harvest in Brazil?

Still, the recovery in Chinese demand may be more than a temporary blip. The China economy is showing green shoots at last after the country’s extended COVID lockdown despite worries a trade war could prolong the decline. Data is still weak as the Communist government beats the drum for expansion, though it has so far refrained from big stimulus measures. Investors apparently believe the market there has turned the corner, amid signs of large inflows from bargain hunters.

The best sign yet for soybean prices comes from China’s huge hog industry, which at long last has begun rebuilding herds. Whether an aging population will belly up to the meat counter is just one dynamic U.S. farmers must watch in hopes that their own fortunes might improve.

.png?width=1280&auto=webp&quality=80&disable=upscale)

Fears drive market weakness

Fears China could lead a global exodus from the U.S. dollar, the world’s reserve currency, were one likely cause of greenback weakness since the first around of new tariffs in February. Though tariffs so far are much lower than threatened, traders turned over any rock they could to look for signs of an impact. That’s one reason the dollar last week struggled to hold support off July lows, sinking the trade-weighted index to the weakest level since February 2022 before rebounding a little.

A dollar downdraft could ripple far and wide, though impacts historically are hard to predict. A weaker dollar tends to boost prices of commodities globally traded in dollars, like crude oil. Impacts on grains are mixed.

Fears tariffs and higher prices could dampen consumer spending also fed bears looking for a recession and the end of U.S. “exceptionalism.”

The cause of the latest handwringing came from Producer Prices, which sometimes provide clues about inflation. Though these numbers are pretty much deep in the weeds of economic data, the PPI reading for July was up a little more than 2%. While that isn’t a big number, it was at the top of the range for the last 30 months and may stem from companies beefing up inventories while trying to front-run tariff exposure.

Odds the Federal Reserve will cut interest rates at its next meeting in September rose, with betting on Federal Funds futures seeing a chance for three cuts of one-quarter of 1% by the end of the year.

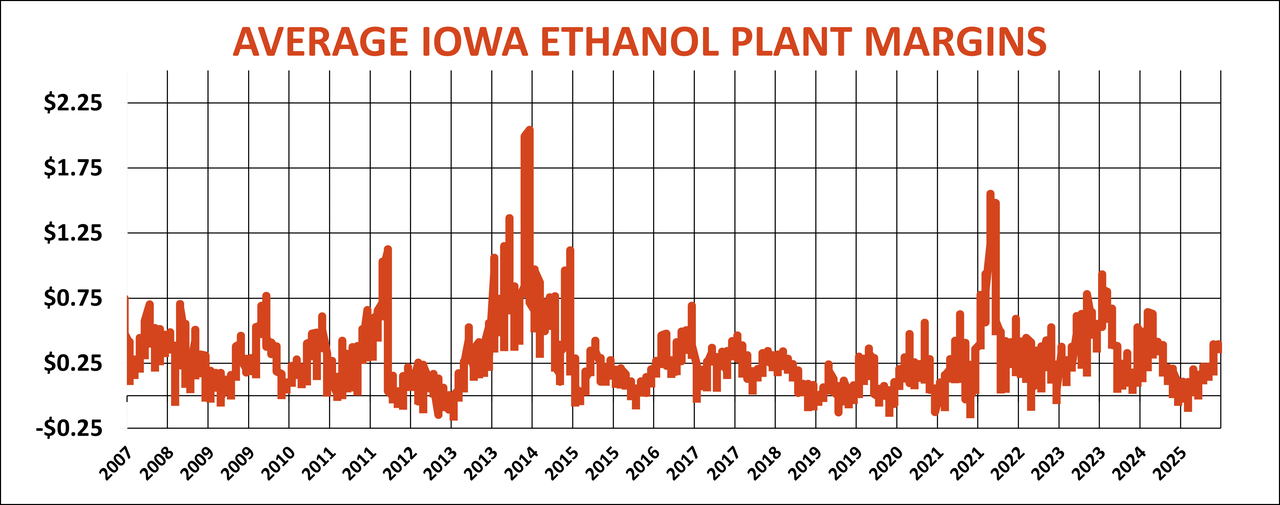

Ethanol Catch 22

A change from corn prices with a $3 or $4 handle could also come from any or all of the three legs of demand for the crop: usage by ethanol plants, livestock feeders or exporters. None appear likely for a major reversal of fortunes, despite increases in the July WASDE that put total usage up around 4% over the previous year.

Lower prices and big crops tend to boost demand, making them a double-edged sword of sorts. Biofuels are the poster child for that dichotomy.

A big increase in consumer confidence – and fatter wallets – could increase petroleum consumption and biofuel blending as drivers hit roads busy with more trucks hauling more goods. But higher energy costs could just as quickly dampen demand, in a classic Catch 22.

Petroleum scarcity could also flow from events on the world stage, a lesson first learned in the inflation-plagued 1970s era of Arab oil embargoes. Middle East peace is still an oxymoron, pinning oil’s future in part to another region riven by war.

The Alaska meeting between President Trump and Russian leader Putin could put more oil on the market, bringing lower costs sought by the American side. But this latest version of détente could also facture relations with Europe, already angered by the on-again, off-again U.S. tariffs. Remember playing poker with all face cards and deuces wild? Even four-of-a-kind was never a sure winner in those playground games.

Feed usage is also improving, though in fits and starts. The U.S. cattle herd is down year-on-year, but sky-high beef prices could lure expansion. A few more hogs showed up at the trough this summer as the poultry industry was ravaged by avian flu. But the number of critters – as defined by USDA’s Grain Consuming Animal Units, is still expected to rise just half of 1%, though consumption per individual could be around 4% higher.

Building barns and breeding cows and sows takes time, so this improvement won’t happen overnight.

Soybean exports can turn quickly

Exports can turn more quickly, especially for soybeans. Lots of places around the world grow corn and other feed grains, but South America and the U.S. still dominate oilseed production.

A drought in either hemisphere can drastically alter the picture, turning all eyes to planting in Brazil, which typically gets underway in mid-September. Parts of northeast Brazil are experiencing more drought than a year ago, but the main center-west region overall looks in good shape so far.

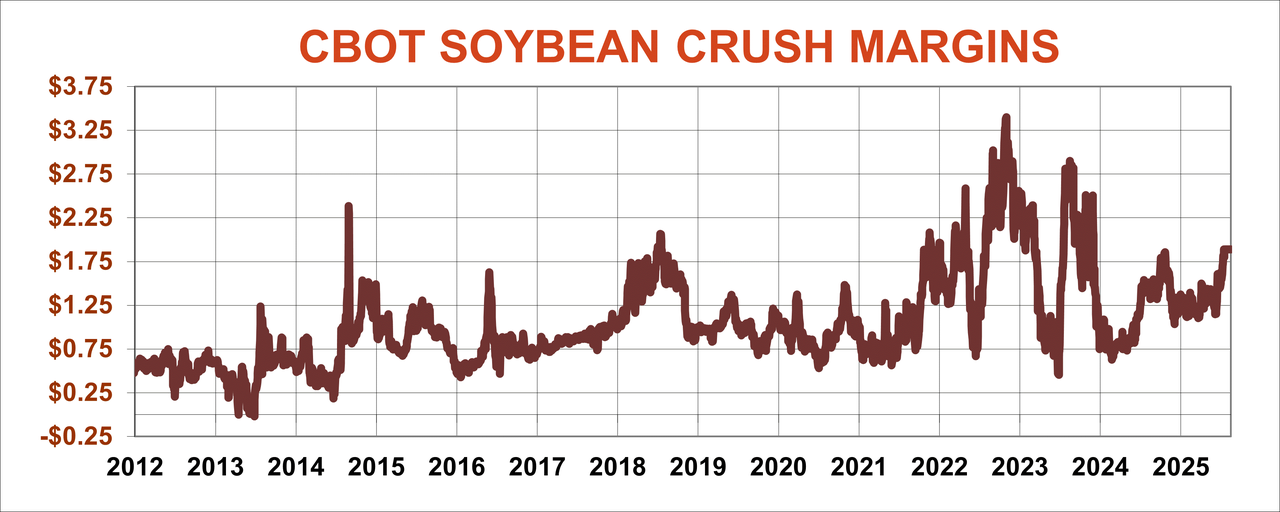

Demand for soybean meal normally influences prices more than oil, but biofuel hopes kept processors running strong. Crush margins are stronger than average as a result, rising steadily throughout the year. Again, that’s a positive, but with climate change an all but forgotten issue, economics, not politics appear likely to set the tone into 2026.

Of course, that’s what farmers have long maintained should happen, if only Washington would keep its nose out of agriculture. We can hope.