Those surprised by this month’s World Agricultural Supply and Demand Estimates report should get ready: Before any possible cuts in the 2025-26 corn crop, the market will likely see the 2024-25 global crop grow bigger and likely set a new record high after Brazilian farmers finish harvesting a massive corn crop.

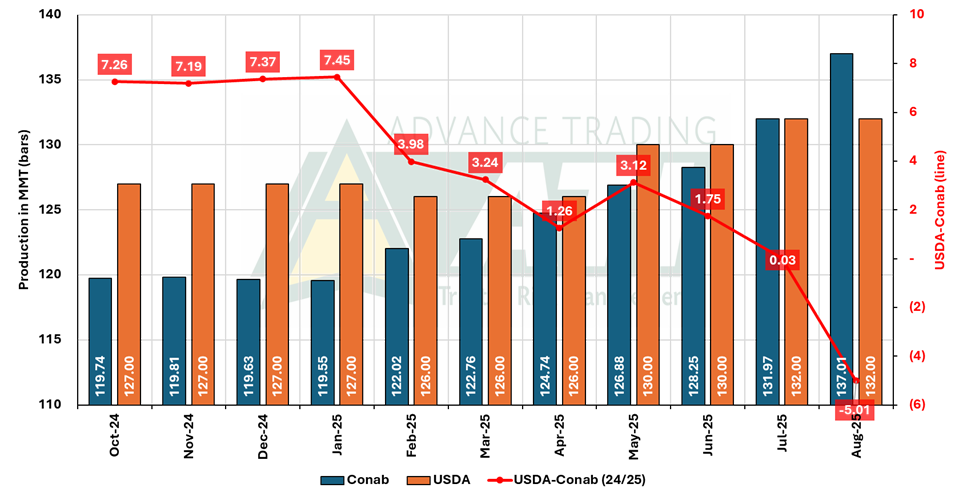

Though Brazil’s second corn crop was nearly 85% harvested last week and sources across the country are reporting higher-than-expected yields, the USDA surprisingly kept its August estimate for Brazil’s production unchanged at 132 million metric tons. Two days after that report, Conab increased its projection for Brazil’s 2024-25 production by nearly 5 MMT, bringing it up to 137 MMT. That’s not only higher than the USDA’s current estimate, but it was also the first time this season that Conab’s forecast has exceeded USDA’s. This is a notable shift on two fronts:

- USDA’s estimate last year was as much as 13 MMT higher than Conab’s at one point.

- Conab’s current projection is now equal to USDA’s record-high estimated production for Brazil in the 2022-23 marketing year.

Favorable weather and record yields in key states such as Mato Grosso, Goiás, and Paraná are leading Brazil to a potential record crop in the 2024/2025 marketing year. The second corn crop, or safrinha, accounts for nearly 80% of Brazil’s total production and has been especially productive. As a result, local consulting firms estimate total production at a massive 150 MMT.

Brazil: Exports moving slow

Despite the bumper harvest, Brazil’s corn exports are off to a slow start. Several factors are contributing to the sluggish pace of Brazilian corn exports:

- China is not buying as aggressively as in previous years. After a strong domestic harvest and large stockpiles, China has significantly reduced its corn imports in 2024-25.

- Domestic demand in Brazil is rising, especially from the expanding corn ethanol industry. Both USDA and Conab have noted a sharp increase in Brazil’s food, seed and industrial (FSI) use, particularly for ethanol production.

- Logistical bottlenecks at ports and limited storage capacity are also playing a role. With soybeans still moving through export channels due to better prices and limited port capacity, corn shipments are being delayed. (Note: Rumors are that Brazilian farmers have been using more silo bags to store corn and soybeans and will likely wait for better prices before they sell more of their crops).

This combination of strong domestic use and weak export momentum could have ripple effects across global markets—especially for the United States.

What it means for U.S. corn exports

USDA raised its forecast for U.S. 2025-26 corn exports from 2.675 to 2.875 billion bushels, citing strong U.S. competitiveness and expectations of relatively low global market prices. However, if Brazil’s export pace picks up later in the year—as it often does—U.S. exporters could face higher competition, particularly in key markets like Southeast Asia and the Middle East.

The first quarter of the marketing year (September-November) will be critical. If Brazil continues to move corn slowly, the U.S. could benefit from early-season demand. However, if Brazilian exports accelerate later in the season, in December through February, they could compete with U.S. shipments during a critical window.

Looking ahead

Much uncertainty remains in the months ahead, as USDA likely will revise its U.S. yield estimate (perhaps downward) and other questions likely will bring additional volatility to the corn futures market. Questions include:

- When will Brazil’s export pace accelerate?

- What will be the effect of ongoing export tariffs on trade?

- Will the U.S. arrange trade agreements with key partners?

- Will China return to the market in a meaningful way?

For now, both the U.S. and Brazil are on track for record or near-record corn crops. Yet, the real story may lie in how—and when—these crops move through global trade channels.