For the second consecutive year, corn futures posted a solid bounce during the crop insurance price discovery period in February. Soybeans joined the rally this year as well, a contrast from 2024 when bean futures largely stayed flat to lower during that same window. Adding fuel to the fire, both markets have continued to climb alongside crude oil since hostilities escalated in Iran.

With growing concern about fertilizer supplies and petroleum shipments disrupted by reduced vessel traffic through the Strait of Hormuz, the question many farmers have is whether these developments will complicate U.S. Spring acreage plans — especially with fieldwork potentially just 45 days away for much of the Corn Belt.

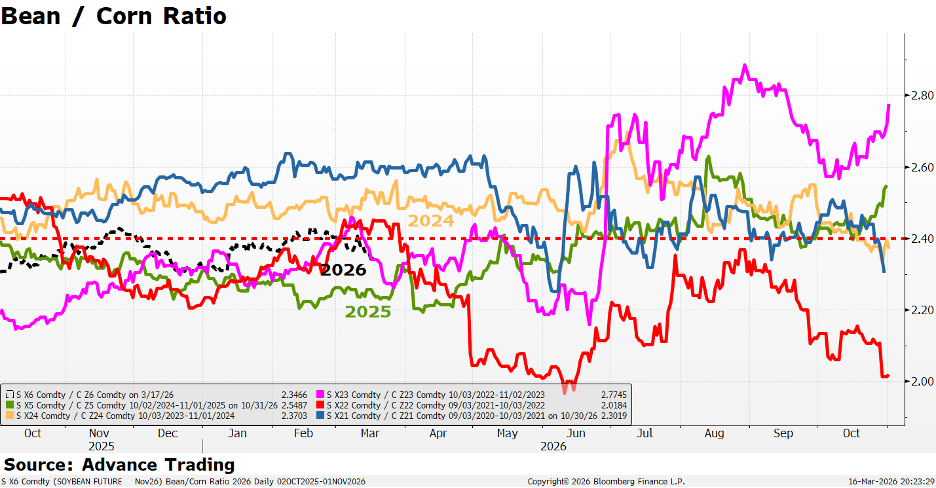

This rally is unfolding at a particularly sensitive time. USDA surveys for the closely watched Prospective Plantings and Grain Stocks reports, scheduled for release March 31, were collected during the first two weeks of this month. As always, the central question heading in is whether we'll see a meaningful shift away from corn acres this spring. The soybean-to-corn price ratio currently sits near 2.35:1, notably higher than a year ago. Historically, a ratio near 2:1 favored corn, while a ratio closer to levels seen in 2021 tends to incentivize producers to plant more soybeans. Where that ratio lands when planting decisions are finalized will carry real weight.

What do these reports do to prices?

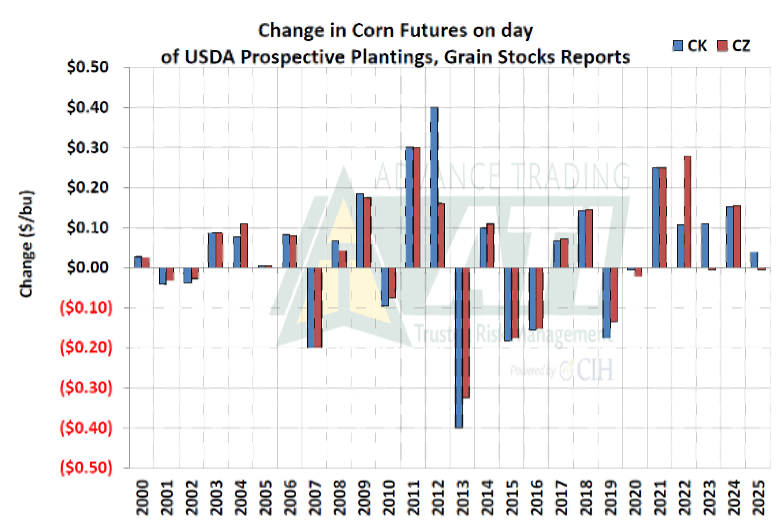

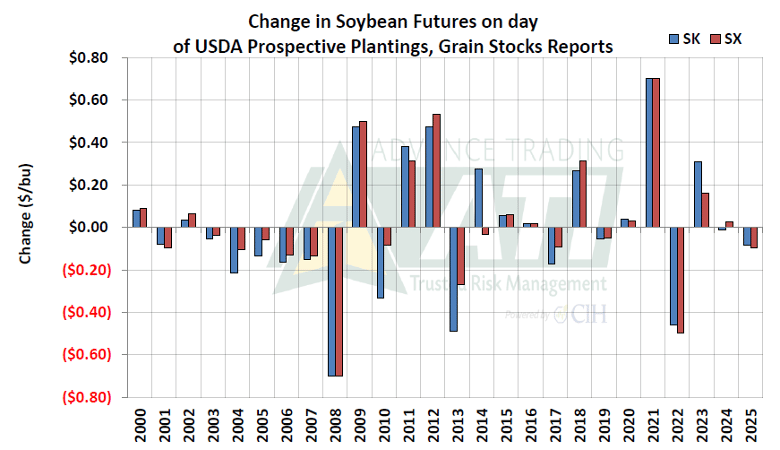

The Prospective Plantings and Grain Stocks reports have a track record of moving markets — sometimes sharply. The charts below capture the one-day price change in both old-crop futures (March contract month "CK" for corn, "SK" for soybeans) and new-crop futures ("CZ" and "SX") on the day each report was released, measured against the prior day's settlement. As a reference point: On March 31, 2022, December corn futures closed nearly 28 cents higher while November soybean futures fell nearly 50 cents.

A few patterns and non-patterns worth noting:

- No year-to-year trend exists. New-crop beans fell roughly 46 cents in 2022, gained 31 cents in 2023, and were nearly unchanged in 2024. Each year stands on its own.

- Old-crop and new-crop prices for the same commodity typically move in the same direction in a given year, but corn and soybeans don't have to — and sometimes don't, as 2022 illustrated.

- The magnitude of moves has generally increased in recent years, reinforcing the financial stakes of being unprepared on report day.

Looking ahead

Whatever happens on March 31, the market has already offered meaningful opportunities to make sales and lock in profitable levels ahead of planting. We are now entering what is historically the most volatile stretch of the marketing year. With that in mind, this is an ideal time to get ahead of the spring rush — consider placing offers now so that if the rally extends, you're positioned to act. December '26 corn futures recently approached $5, with December '27 near $4.90; November '26 soybeans were near $11.75, and November '27 beans topped out this month around $11.21.

One final reminder: Acreage estimates printed on March 31 can — and do — get revised significantly. Last year was a prime example, with notable adjustments surfacing in the June report and again in the final acreage figures. Stay prepared, stay proactive, and here's hoping for ideal field conditions just around the corner.

Brett Mapel is a risk management consultant at Advance Trading Inc.