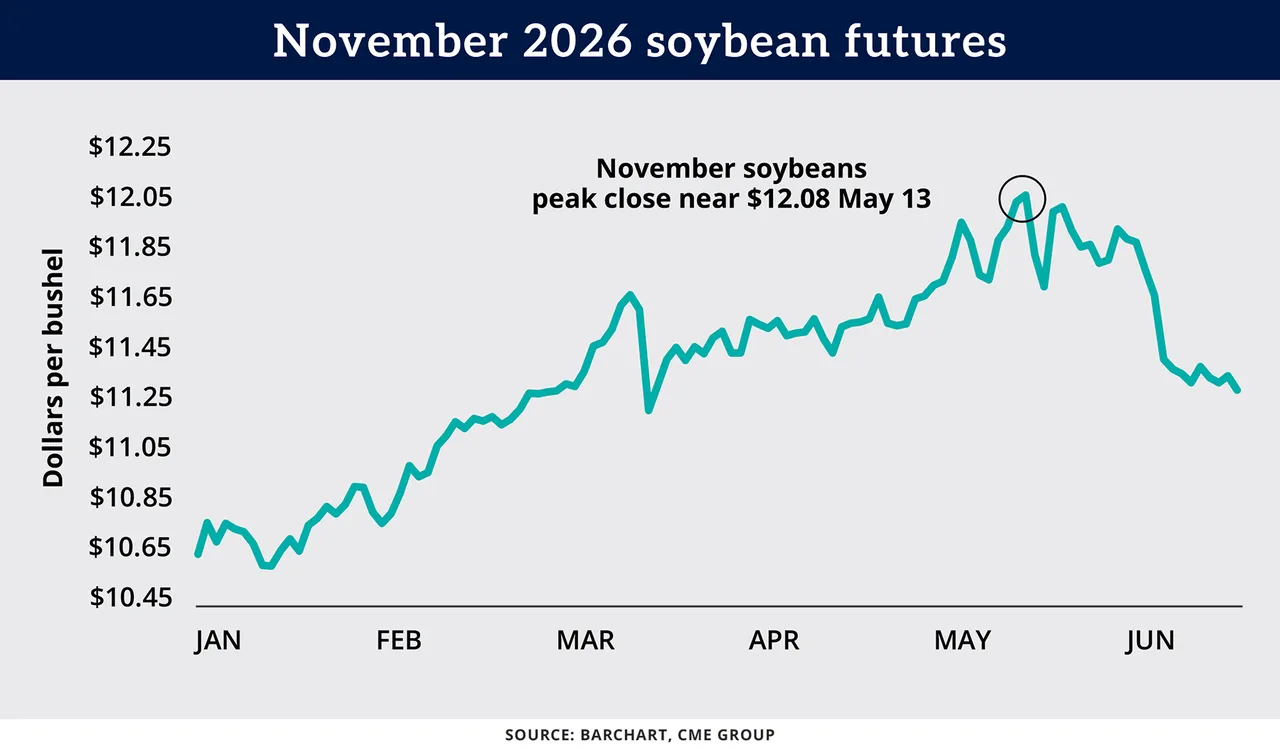

A soybean market that showed impressive resilience much of this year appeared to reach a crossroads as the first half of June unfolded.

The brisk planting season followed by widespread rains and mostly crop-favoring weather across the Midwest took a lot of the wind out of bulls’ sails, sending futures prices tumbling from two-year highs above $12 per bushel in May.

Mid-June brought more grist for the mill, including USDA’s World Agricultural Supply and Demand Estimates report that did no favors for bulls. Perhaps a more significant near-term development, however, came with a long-awaited U.S.-Iran agreement to, at some point any day now, finally end the war. That was enough to send crude oil futures to three-month lows and likely remove one of the key bullish props for soybeans this year.

Would a crude oil return to pre-war per-barrel levels in the $60s spell downside doom for beans? Not necessarily. Note that as of mid-June, soy oil futures were still trading near four-year highs as the biofuels boom remained in full force.

Crude oil’s path, U.S.-Iran deliberations and how long it takes to untangle the Strait of Hormuz are all worth tracking in the weeks ahead. But a few other factors loom larger. First, a quick recap of the June WASDE report:

U.S. supplies not tight or excessive but getting snugger. USDA kept 2025-26 U.S. ending soybeans stocks unchanged at 340 million bushels, contrary to expectations for a small cut. The agency also held 2026-27 ending stocks steady, but at a somewhat tighter 310 million bushels.

Exports docked further. USDA lowered 2025-26 soybean exports for the second month in a row, dropping its estimate 20 million bushels to 1.51 billion bushels, a 13-year low. Crushing for 2025-26 was raised slightly, and for 2026-27, held at 2.75 billion bushels, a record for the sixth year in a row.

Even bigger hill of beans in South America. USDA kept its 2026 soybean harvest estimate for Brazil unchanged at a record 180 million metric tons (6.61 billion bushels) but raised Argentina’s crop by 2 MMT, or 4.2%, to 50 MMT. That led to a slight increase in global supplies.

Soybean futures extended a monthlong downslide following the June 11 report but didn’t suffer anything close to the severe fund liquidation downdraft seen in the corn market. Speculators still see reasons to be long in soybeans as well as soy oil. That’s a bull story that still has legs.

But be sure to circle June 30 on your calendars. That’s when USDA releases its annual survey-based Acreage update, and the numbers, combined with Midwest weather, promise to set the market’s tone for the rest of the summer.

A year ago, USDA slashed 960,000 soybean acres from its March Prospective Plantings forecast, dropping planted acreage to 82.5 million. (USDA eventually lowered 2025 acreage to 81.2 million.) The acreage cut sparked a brief rally of about 34 cents in November 2025 soybean futures.

It’s probably not wise to count on a similarly bullish surprise this year. Many analysts expect USDA to boost soybean plantings by 1 million to 2 million acres from the 84.7 million acres predicted in March, based on beliefs that a war-driven surge in fertilizer costs prompted many farmers to shift land away from corn.

It’s unclear how widespread such a shift may have been, and whether it would result in meaningfully higher or lower corn or soybean plantings compared to the March forecasts. But another 1 million acres or so of beans, combined with ample rains and a relatively mild summer many forecasters anticipate, could easily result in a record crop. At 84.7 million acres, we’re already close.

Last month, USDA estimated 2026-27 U.S. soybean production at 4.435 billion bushels, just 29 million bushels below the 2021 record, and forecast the average 2026 yield at 53 bushels per acre, matching 2025’s record.

For farmers contemplating pricing opportunities, it’s a good idea to prepare for a bearish surprise on June 30 that could send November soybeans tumbling back near or below $11 (futures traded around $11.35 as of mid-June). But be on the lookout for opposing scenarios, too – if the additional acres aren’t there as many think, the market could take a quick elevator ride back up near $12.