Markets hate uncertainty, which is why nothing roils prices like the fog of war. Unintended consequences and collateral damage usually follow the missiles and bombs, and predicting the fallout is difficult at best.

So, it was inevitable the new war with Iran rattled more than windows throughout the Middle East. Impacts spread beyond the energy market, where U.S. crude oil prices surged more than 60% even though production in North America was safe. In fact, output here could even benefit from the conflict because it gave drillers in the Permian Basin a chance to hedge new wells at profitable prices.

Sometimes the moves caused head-scratching. Gold normally benefits in times of trouble and even of the beleaguered U.S. dollar found strength, at least temporarily. But both “safe havens” also sold off at times because their owners had to raise cash to pay margin calls in other markets, with the bond market pressured further by fears of inflation rekindled by higher fuel costs.

Corn and soybeans rallied to end the week as traders waited nervously for news from a White House famous for social media posts at times when others are enjoying time off — or at least trying to. Motivation for the rally came from the fundamentals of supply and demand as well as so-called technicals based on price chart patterns that flashed “buy” signals after nearby corn held a gap at $4.40 and soybeans bounced off support from a steep uptrending channel.

Whatever the cause, futures rallied well into the top third selling ranges from my forecasting model, a reminder to price 2025 inventory and 2026 production if your farm’s margins won’t handle a pullback.

Money flow and prices

It’s also prudent to dig down in the weeds to find clues about what’s happening. I look at two sources in particular: money flows from big players tracked by the Commodity Futures Trading Commission and its Commitment of Traders, and the relationship between prices of different commodities.

The CFTC puts out a series of commitments each week, but I focus on positions of speculators and commercials such as grain merchandisers found in the so-called “legacy reports” over the past year.

Some of these relationships are easy to explain. Buying or selling of corn tends to move hand-in-hand with positions of these players in ethanol. That is, when funds are buying corn, they’re also buying biofuel, and vice versa. But both corn and soybeans tend to have an inverse relationship with livestock: Big traders buy grains when selling meats — locking in their cost of gain and expected revenue.

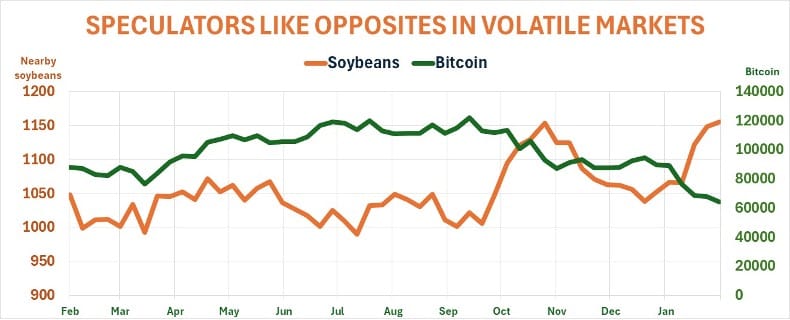

This tit-for-tat only goes so far, notably for positions in metals. When players decrease ownership in gold they tend to add soybean contracts, but they also buy both corn and the precious metal.

Financial contracts likely show the most divergence in these Commitments. For example, when players sell soybeans they tend to buy dollars, the stock market, dollars and Bitcoin. And the opposite is true for corn.

Positions and prices

Not surprisingly, these moves drive prices. This appears particularly true for corn and soybeans, where correlations between commitments and prices is around .9 — remember, 1 is a perfect correlation and 0 means no relationship.

Commitments aside, moves in corn and soybean futures sometimes follow different drummers, too. While it may seem like corn and soybeans move in tandem, statistically this is not the case — the correlation between prices of the two is small. And negative correlations appear true for corn prices and many financial and precious metals contracts.

Though corn tends to go down when gold rallies, soybeans do the opposite, and similar patterns can be seen in silver, platinum, palladium, aluminum and copper. The same is true for financial assets, notably the dollar, Treasuries and the S&P 500 Index. It’s unclear why corn would go down when stocks and soybeans rally. Of course, these patterns aren’t perfect. The stock market sold off hard as crude oil rallied to end last week, but soybeans continued on a tear, in part because of claims by the Trump Administration that China was due to ramp up its buying.

Another reason both corn and soybeans took off last week came from the conflict with Iran. Most of the headlines were on energy, but another key export out of the Persian Gulf also ground to a halt: Fertilizer, notably urea. Prices exploded higher and not just in the Middle East. While the U.S. doesn’t import significant amounts out of the Strait of Hormuz, fertilizer is an international market, which sent the cost of urea at the Gulf — the U.S. Gulf — on a tear, jumping more than 25% in just two days, similar to the move by prices out of the Middle East.

Still, some traders believe markets could quickly settle back, as long as the conflict winds down fairly quickly. They point to “backwardation,” a term that’s the opposite of the “carry” seen in grain markets with a surplus. Nearby energy prices have been higher than deferred contracts, a hint the market was worried about prices right now, not a few months into spring.

Trouble is, no one knows how long the bombs will fly, much less whether a messy civil war could erupt between supporters of clerics and those who protested vehemently for reforms. One thing seems likely: The longer peace takes, the more rattled investors may avoid anything with a whiff of risk, from stocks to soybeans.