While money may be “the mother’s milk of politics,” the lifeblood of markets is the data put out by governments and organizations. Traders of everything from stocks to soybeans jump on these numbers, driving prices up or down in an instant.

But a blizzard of reports released in the last week or two barely moved the needle. March World Agricultural Supply and Demand Estimates from USDA and conflicting readings on the U.S. economy failed to elicit much excitement.

The problem was not with the numbers, but when they were collected, which was before the war with Iran. That made any attempts to base forecasts on these reports seemingly irrelevant. Would the conflict change the outlook, say for inflation or soybean exports? That appears to depend on how long the bombs keep falling and how the aftermath plays out — questions that provoke plenty of opinions but few hard facts.

Still, risk premiums ratcheted higher, most notably in energy contracts, where crude oil flirted with $100 a barrel. And, though Iran isn’t blocking many — if any — shipments of soybeans through the Strait of Hormuz, futures traded these headlines like summer weather forecasts.

The connection between energy and grain markets was hardly an outlier. Over the past 15 years crude explained almost half the variance in soybeans, and nearly as much in corn. The connection topped 60% with all food prices worldwide. Correlations with soybean oil were even stronger, one reason the product was the driver in soybean futures.

Indeed, in the absence of updated data, one way to gauge potential impacts was to look at connections between a variety of markets in the past. Here’s what this early warning system says to watch:

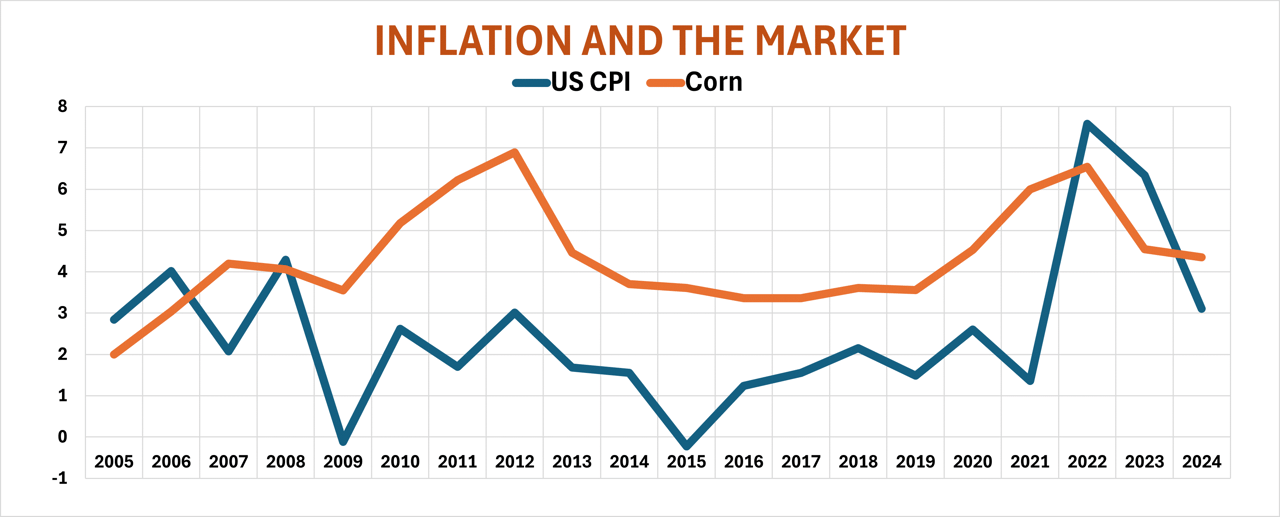

Inflation flags

The Consumer Price Index and other data suggest higher prices are proving “sticky” — that is, while inflation isn’t out-of-control, it is staying elevated, in part because wages remain strong even if companies aren’t adding new employees.

The cost of food is a major component of inflation gauges, and higher food prices are associated with rising CPI, along with higher prices for corn and soybeans. The opposite is also true, so weaker inflation could mean lower grain markets, too.

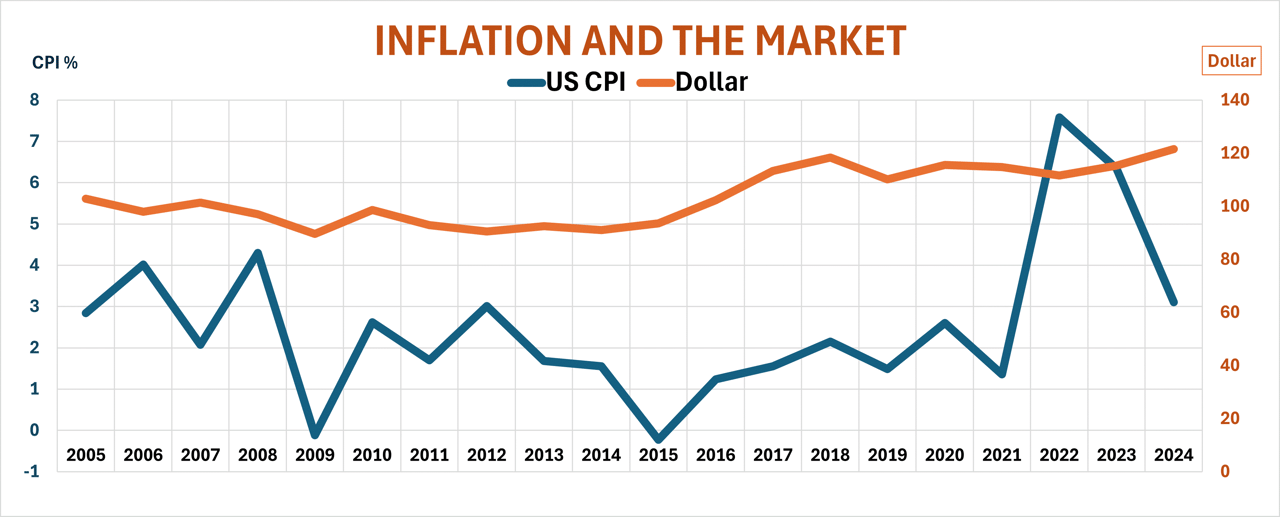

Dollar dilemma

After falling to four-year lows in January, the dollar surged to its best showing in almost a year as worried investors fled to the greenback as a safe haven from the storm in the Middle East. The move was a caution flag for traders because over the past 15 years a stronger currency meant lower grain prices.

From a longer perspective, however, the impact was different. Over the past 50 years a stronger dollar was associated with higher grain markets, perhaps because support for the greenback meant a better economy that gave consumers more funds to buy food.

The trick for traders is to correctly pick which trend is playing out now, a selection that may be proven only in hindsight.

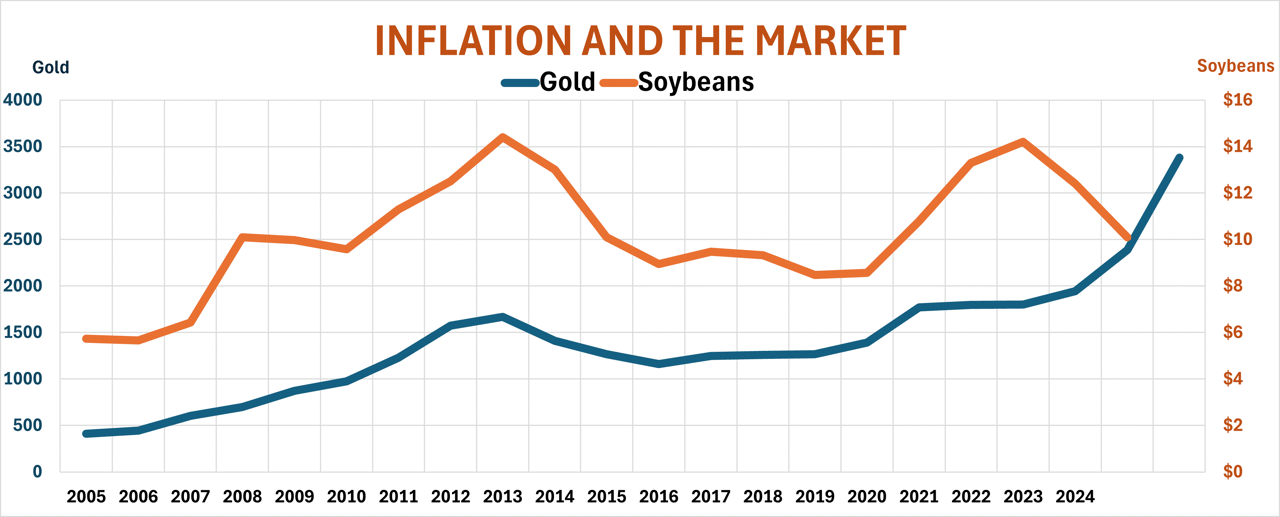

Gold rush

The other safe haven of choice in the wake of the Iran war was a traditional store of value: gold. Over the past 15 years the precious metal has a decent correlation with grain and food prices, and that statistical connection was twice as strong when the past 50 years are measured. The correlation is positive – that is, both gold and grains tend to move in the same direction, both up and down.

The takeaway: In times of trouble gold glitters and food becomes just as precious. That was true 5,000 years ago, and it still holds today, in the age of digital currencies and electronic payments.

Growth is good

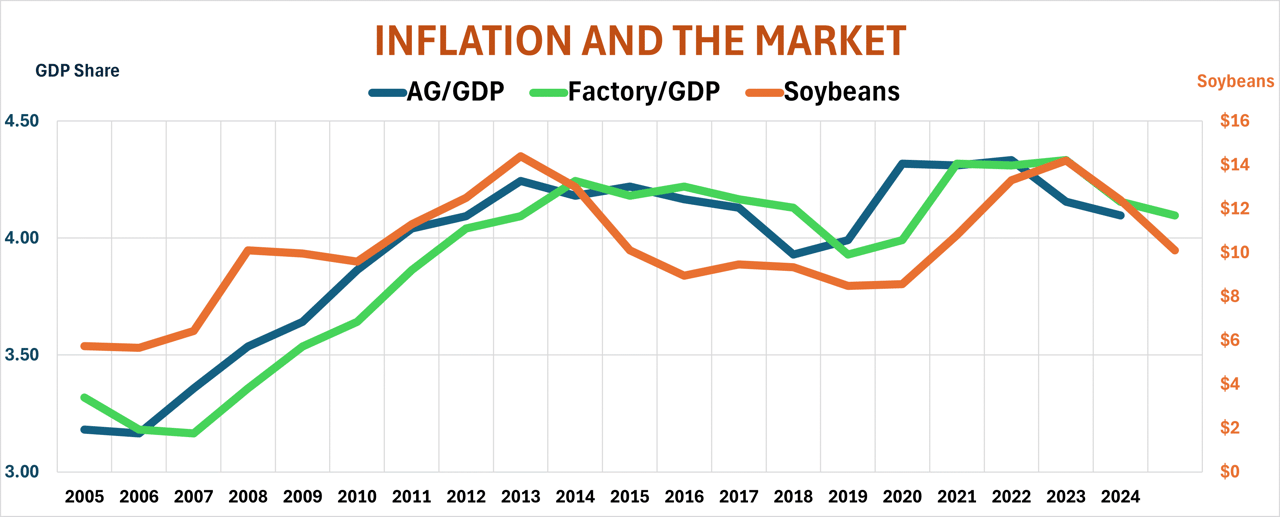

Sharply higher energy prices raised fears of a recession, or even a repeat of the stagflation of the 1970s, when inflation accompanied poor growth. Over the past 15 years economic activity went hand-in-hand with higher grain and food markets. But when GDP growth is tracked over the past 50 years, this correlation evaporates, suggesting sluggish growth may not be terrible for prices, either.

Watch the health of the nation’s factories for signals. Rising manufacturing is normally good for prices, but not if it increases faster than the agricultural sector. When factories boom more than fields, grain markets and food prices tend to lag behind.

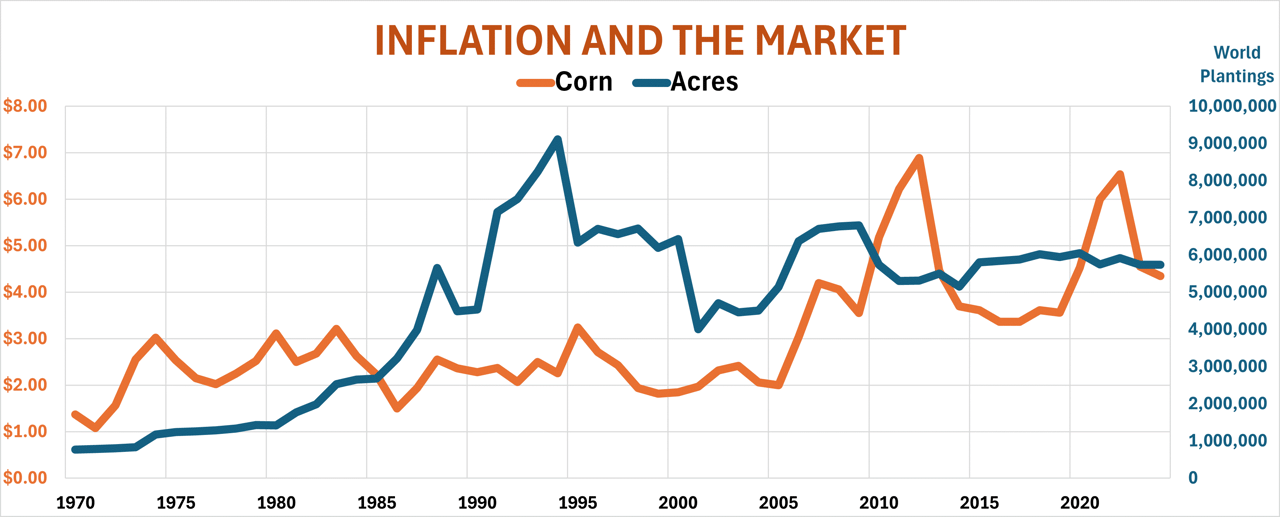

Acres mean output

You can’t sell what you don’t plant, and lower crop acreage around the world indeed is associated with higher prices for grains and food. At least, that’s been the trend over the past 15 years. Going back 50 years tells the opposite story.

Financial constraints and changing government programs may be the difference for current farmers. In the past high grain prices occurred even when farmers were expanding acreage. Today’s just-in-time economics may give farmers greater flexibility to shift rotations or let some ground lie fallow if they can’t lock in profits.

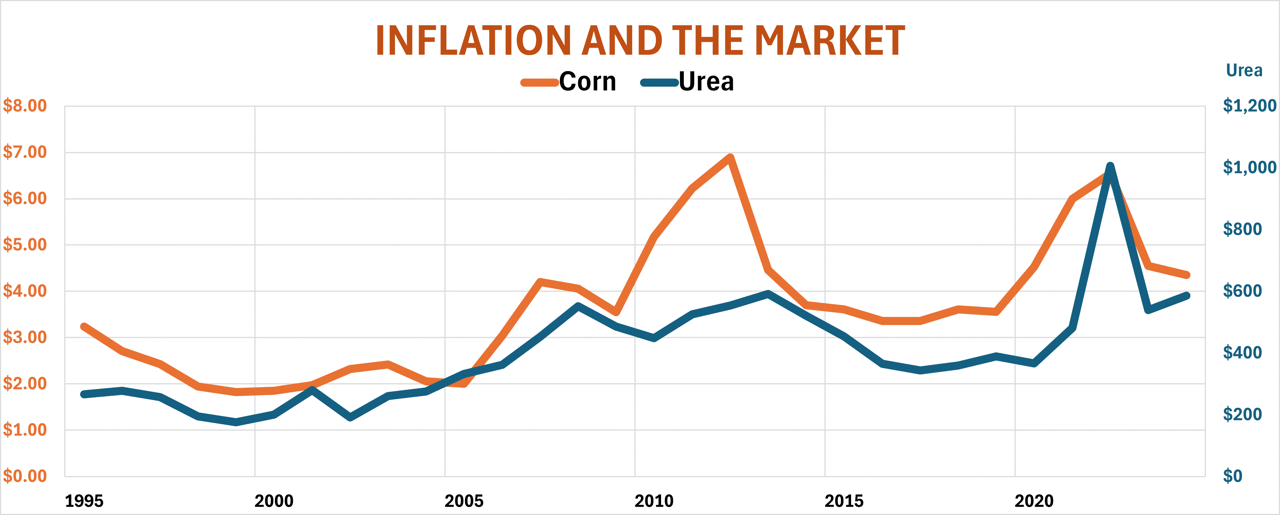

Fertilizer frenzy

That just-in-time trend could cause a major, unintended consequence of the war: sharply higher fertilizer costs. Growers who put down nutrients last fall or locked in prices and/or supplies over the winter may be at a significant advantage as planting starts this spring. The Iran conflict not only spurred a rally in natural gas, the feed stock for many nitrogen compounds, but the new war also choked off shipments of fertilizers, sending urea at the U.S. Gulf to $600 a ton, 80% higher than the cost last fall.

Higher fertilizer prices are often associated with higher food and grain prices. This could be a chicken-or-egg debate in 2026. Higher grain and food prices give farmers more incentive to add nutrients, but higher fertilizer values can also make it harder to maintain applications, boosting crop prices if production suffers as a result.